Annual budgeting provides a fixed financial plan for the year, allowing organizations to allocate resources with clear targets and control. Rolling budgeting offers ongoing adjustments based on real-time data, promoting flexibility and more accurate forecasting. Choosing between the two approaches depends on the need for stability versus adaptability in money management.

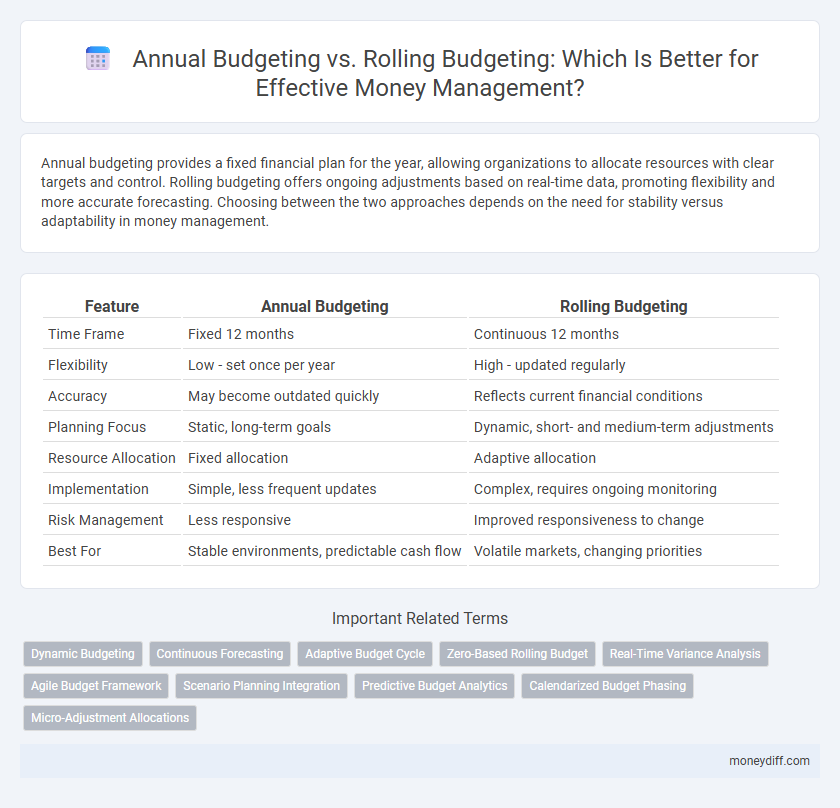

Table of Comparison

| Feature | Annual Budgeting | Rolling Budgeting |

|---|---|---|

| Time Frame | Fixed 12 months | Continuous 12 months |

| Flexibility | Low - set once per year | High - updated regularly |

| Accuracy | May become outdated quickly | Reflects current financial conditions |

| Planning Focus | Static, long-term goals | Dynamic, short- and medium-term adjustments |

| Resource Allocation | Fixed allocation | Adaptive allocation |

| Implementation | Simple, less frequent updates | Complex, requires ongoing monitoring |

| Risk Management | Less responsive | Improved responsiveness to change |

| Best For | Stable environments, predictable cash flow | Volatile markets, changing priorities |

Understanding Annual Budgeting: Definition and Process

Annual budgeting involves setting a fixed financial plan for a 12-month period, outlining expected revenues, expenses, and cash flow to guide money management. The process includes detailed forecasting, allocation of resources, and approval cycles to ensure alignment with organizational goals. This approach emphasizes stability and accountability but may lack flexibility to adapt to unforeseen changes in the financial environment.

Exploring Rolling Budgeting: A Dynamic Approach

Rolling budgeting offers a dynamic approach to financial planning by continuously updating budget forecasts, typically on a monthly or quarterly basis. This method enhances responsiveness to market changes and operational shifts, providing real-time alignment with organizational goals. Companies adopting rolling budgets experience improved accuracy in cash flow management and more agile resource allocation compared to static annual budgets.

Key Differences between Annual and Rolling Budgets

Annual budgeting sets a fixed financial plan for a 12-month period, providing stability and clear targets but often lacks flexibility to adapt to changes. Rolling budgeting continuously updates the budget by adding a new period, usually a month or quarter, as the current period ends, promoting agile money management. Key differences include the fixed timeframe and less responsiveness of annual budgets versus the ongoing adjustments and enhanced accuracy found in rolling budgets.

Pros and Cons of Annual Budgeting

Annual budgeting provides a clear financial framework with fixed targets, aiding long-term strategic planning and control over expenditures. However, its rigidity can limit responsiveness to market fluctuations or unexpected expenses, potentially causing resource misallocation. The static nature of annual budgets often results in delayed adjustments, which may hinder timely decision-making in dynamic business environments.

Advantages and Limitations of Rolling Budgeting

Rolling budgeting offers continuous updates to financial plans, enhancing adaptability to market changes and improving cash flow management through regular revisions. It allows organizations to respond swiftly to new opportunities or risks, maintaining alignment with strategic goals while providing more accurate forecasts. Limitations include increased administrative effort and potential complexity in maintaining frequent budget updates, which may strain resources and cause forecasting challenges in highly volatile environments.

Impact on Financial Planning and Forecasting

Annual budgeting provides a fixed financial framework, enabling organizations to set clear targets and allocate resources for the entire fiscal year, but it can limit responsiveness to market changes. Rolling budgeting continuously updates projections by incorporating recent financial data, enhancing accuracy in forecasting and flexibility in reallocating funds to meet evolving business needs. This dynamic approach improves financial planning by allowing timely adjustments and better alignment with real-time performance metrics.

Adaptability to Economic Changes

Annual budgeting provides a fixed financial plan that may lack flexibility to respond to sudden economic shifts, often leading to misaligned resource allocation. Rolling budgeting continuously updates forecasts and allocations, allowing organizations to adapt their financial strategies in real-time as market conditions evolve. This adaptability enhances financial resilience and improves decision-making accuracy during periods of economic uncertainty.

Best Practices for Implementing Each Budgeting Method

Annual budgeting requires setting clear financial goals and detailed expense planning at the start of the fiscal year, ensuring alignment with organizational priorities and maintaining strict monitoring to detect variances early. Rolling budgeting demands continuous updating of forecasts, frequent review cycles, and agile adjustments to reflect changing market conditions and operational realities, promoting flexibility and real-time resource allocation. Best practices involve leveraging accurate data analytics, engaging cross-functional teams for insights, and integrating budgeting software to enhance precision and collaboration in both approaches.

Choosing the Right Budgeting Method for Your Financial Goals

Annual budgeting provides a fixed financial plan for a 12-month period, enabling clear goal setting and expense control based on projected revenues and costs. Rolling budgeting continuously updates the financial plan, typically monthly or quarterly, incorporating real-time data to adapt to changing business conditions and improve forecasting accuracy. Selecting the right budgeting method depends on your financial goals, with annual budgeting favoring stability and predictability, while rolling budgeting supports flexibility and responsiveness in money management.

Future Trends in Money Management Budgeting Strategies

Annual budgeting remains popular for its straightforward, fixed framework, but rolling budgeting is gaining traction due to its flexibility and ability to adapt to rapid market changes. Future trends in money management emphasize increased use of rolling budgets integrated with real-time data analytics and AI-driven forecasting, enabling more accurate and dynamic financial planning. Organizations adopting rolling budgets benefit from enhanced agility and improved responsiveness to economic fluctuations and business growth opportunities.

Related Important Terms

Dynamic Budgeting

Dynamic budgeting through rolling budgeting continuously updates financial plans based on real-time data, offering greater flexibility and responsiveness compared to static annual budgeting. This approach enables organizations to adapt quickly to market changes, optimize cash flow management, and improve forecasting accuracy throughout the fiscal year.

Continuous Forecasting

Annual budgeting provides a fixed financial plan for a specific fiscal year, often leading to limited flexibility in adapting to market changes. Rolling budgeting enhances money management through continuous forecasting, allowing organizations to update projections regularly and respond swiftly to financial fluctuations.

Adaptive Budget Cycle

An adaptive budget cycle emphasizes rolling budgeting by continually updating financial forecasts based on real-time data, allowing for greater flexibility and responsiveness to market changes compared to the static nature of annual budgeting. This dynamic approach enhances money management by aligning budget allocations with evolving business conditions, improving accuracy and resource utilization.

Zero-Based Rolling Budget

Zero-based rolling budgeting enhances financial control by requiring all expenses to be justified from scratch for each period, ensuring allocation aligns precisely with current business priorities. This dynamic approach combines the continuous update feature of rolling budgets with the cost-efficiency focus of zero-based budgeting to optimize cash flow and resource management.

Real-Time Variance Analysis

Annual budgeting provides a fixed financial plan for the fiscal year but often lacks flexibility in responding to market changes, limiting the effectiveness of real-time variance analysis. Rolling budgeting enables continuous updates and adjustments, allowing businesses to perform real-time variance analysis regularly for more accurate money management and better financial control.

Agile Budget Framework

Annual budgeting provides a fixed financial plan for a fiscal year, limiting flexibility in rapidly changing markets, while rolling budgeting involves continuous updates, promoting adaptive financial management aligned with agile methodologies. The Agile Budget Framework leverages rolling budgets to enhance responsiveness, enabling organizations to reallocate resources dynamically and improve forecasting accuracy based on real-time financial data.

Scenario Planning Integration

Annual budgeting provides a fixed financial framework for a fiscal year, enabling scenario planning with predefined parameters, while rolling budgeting continuously updates forecasts and adjusts financial plans to reflect real-time market changes, enhancing responsiveness to evolving scenarios. Integrating scenario planning in rolling budgets allows organizations to dynamically allocate resources and mitigate risks by modeling multiple future conditions with greater accuracy.

Predictive Budget Analytics

Annual budgeting provides a fixed financial plan based on historical data, often lacking flexibility in adapting to market changes, while rolling budgeting continuously updates forecasts to reflect real-time data and trends. Predictive budget analytics enhances rolling budgeting by leveraging advanced algorithms and data models to accurately anticipate future expenses and revenues, improving money management precision.

Calendarized Budget Phasing

Annual budgeting segments financial plans by fixed calendar periods, enabling structured allocation and expense tracking, but may lack flexibility to adapt to changing market conditions. Rolling budgeting continuously updates the budget at regular intervals, such as monthly or quarterly, allowing dynamic calendarized budget phasing that aligns spending with real-time business performance and cash flow needs.

Micro-Adjustment Allocations

Annual budgeting sets fixed financial targets for a fiscal year, limiting flexibility in micro-adjustment allocations, whereas rolling budgeting continuously updates forecasts, allowing dynamic redistribution of resources based on real-time financial performance. Rolling budgeting enhances money management by enabling precise micro-adjustments that align with evolving business conditions and mitigate risks associated with rigid annual plans.

Annual Budgeting vs Rolling Budgeting for money management. Infographic