Monthly budgets provide a comprehensive overview of all expenses and income within a calendar month, helping track bills and fixed costs. Paycheck budgets break down finances based on each paycheck received, enabling more precise control over spending between pay periods. Using a paycheck budget can prevent overspending early in the month, while a monthly budget ensures all obligations are accounted for.

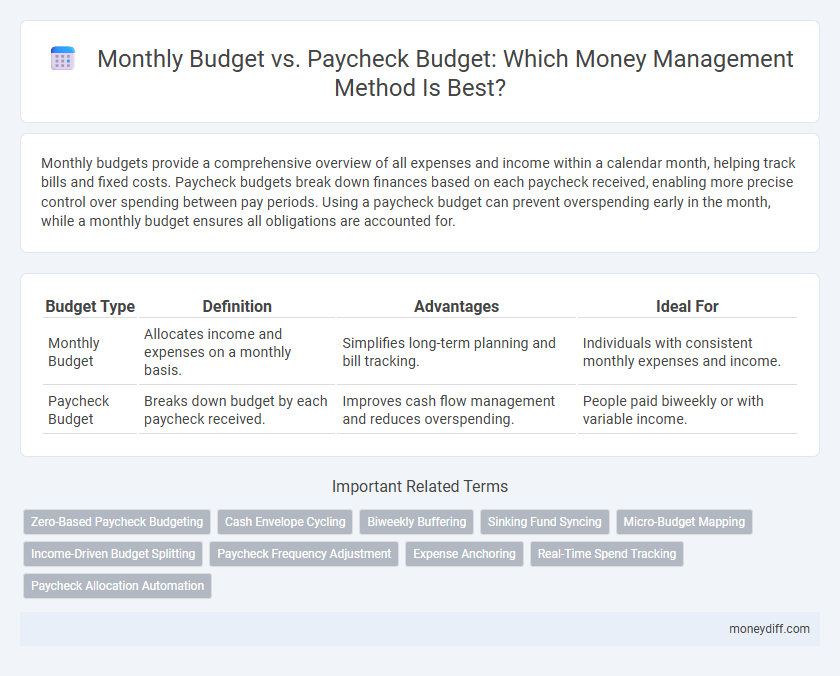

Table of Comparison

| Budget Type | Definition | Advantages | Ideal For |

|---|---|---|---|

| Monthly Budget | Allocates income and expenses on a monthly basis. | Simplifies long-term planning and bill tracking. | Individuals with consistent monthly expenses and income. |

| Paycheck Budget | Breaks down budget by each paycheck received. | Improves cash flow management and reduces overspending. | People paid biweekly or with variable income. |

Introduction to Monthly and Paycheck Budgeting

A monthly budget allocates income and expenses based on a full calendar month, offering a broad overview of financial obligations such as rent, utilities, and subscriptions. In contrast, a paycheck budget divides income by each pay period, allowing for more granular control and immediate expense tracking aligned with actual cash flow. Employing both strategies enhances money management by balancing long-term planning with short-term spending awareness.

Understanding Monthly Budgets

Understanding monthly budgets involves allocating income to cover fixed and variable expenses within a 30-day cycle, ensuring all bills and savings goals are met consistently. Paycheck budgeting breaks down the budget into smaller segments tied to each paycheck, promoting disciplined spending and helping avoid cash shortages between pay periods. Comparing both, monthly budgets provide a big-picture financial overview, while paycheck budgets offer granular control for managing cash flow effectively.

What is a Paycheck Budget?

A paycheck budget allocates expenses based on each individual paycheck rather than the entire month's income, helping to manage cash flow more precisely. It breaks down bills, savings, and spending into segments aligned with pay periods, often biweekly or monthly, ensuring money is available when needed. This approach minimizes overspending and enhances control by syncing financial commitments directly with income timing.

Key Differences: Monthly vs Paycheck Budgets

A monthly budget aggregates all income and expenses for the entire month, providing a broad perspective on cash flow and long-term financial planning. In contrast, a paycheck budget breaks down expenses based on individual paychecks, allowing for more precise control and flexibility with funds throughout the pay period. Key differences include timing, cash flow management, and the ability to adjust spending habits more frequently with a paycheck budget compared to the more static monthly budget.

Pros and Cons of Monthly Budgeting

Monthly budgeting provides a comprehensive overview of income and expenses, allowing for long-term financial planning and better tracking of bills that occur infrequently. However, it can be challenging to maintain accuracy due to fluctuating monthly expenses and inconsistent cash flow, which may cause budgeting errors. The less frequent review cycle may delay necessary adjustments compared to paycheck budgeting, potentially leading to overspending.

Advantages and Drawbacks of Paycheck Budgeting

Paycheck budgeting offers the advantage of aligning spending directly with income cycles, which can reduce the risk of overspending and improve cash flow management by breaking down expenses into smaller, more manageable segments. However, this approach may complicate long-term financial planning and savings goals because it focuses on short-term income allocation rather than the entire month's financial needs. The variability in paycheck amounts, especially for salaried individuals with irregular hours or commissions, can also limit the effectiveness of paycheck budgeting.

Which Budget Method Fits Your Lifestyle?

Monthly budgets provide a comprehensive overview of all income and expenses over 30 days, helping individuals track long-term financial goals and bills with fixed due dates. Paycheck budgets focus on managing funds within each pay period, promoting disciplined spending and immediate allocation of money toward essentials and savings after each paycheck. Choosing between these methods depends on lifestyle factors such as income frequency, spending habits, and financial priorities, ensuring better money management tailored to individual cash flow patterns.

Adapting Your Budgeting Strategy

Adapting your budgeting strategy involves choosing between a monthly budget and a paycheck budget based on your income flow and spending habits. A monthly budget offers a comprehensive overview of expenses due throughout the month, ideal for fixed incomes and predictable bills. In contrast, a paycheck budget breaks expenses into manageable segments aligned with each paycheck, providing flexibility and better control for irregular or biweekly income schedules.

Common Mistakes with Both Budgeting Methods

Common mistakes in monthly budget planning include underestimating irregular expenses and failing to adjust for fluctuating income, leading to overspending and stress. Paycheck budgeting often results in inconsistent saving habits and neglects long-term financial goals due to its focus on immediate funds. Both methods require careful tracking and flexibility to avoid cash flow problems and ensure effective money management.

Final Tips for Effective Money Management

Creating a monthly budget offers a comprehensive view of income and expenses, enabling better long-term financial planning, while a paycheck budget helps control spending between paychecks by allocating funds immediately after each payment. Prioritize tracking all expenses and adjust categories regularly to reflect changing financial goals and avoid overspending. Use automated savings tools and set clear spending limits per category to maintain discipline and improve overall money management effectiveness.

Related Important Terms

Zero-Based Paycheck Budgeting

Zero-based paycheck budgeting allocates every dollar of income to specific expenses, savings, or debt repayment, ensuring no money is left unassigned and maximizing financial control each pay period. This method contrasts with monthly budgeting by focusing on individual paychecks, allowing for more precise cash flow management and preventing overspending throughout the month.

Cash Envelope Cycling

Monthly budget planning allows for broader expense tracking, while paycheck budgeting focuses on managing funds per income cycle to prevent overspending; implementing cash envelope cycling enhances control by allocating specific cash amounts to each spending category, reducing the risk of debt and improving financial discipline. This method ensures timely replenishment of envelopes with each paycheck, fostering consistent savings habits and optimal cash flow management.

Biweekly Buffering

Biweekly buffering aligns income and expenses by dividing monthly bills into biweekly payments, reducing cash flow gaps and lessening financial stress. This strategy enhances money management by creating a buffer that prevents overdrafts and ensures bills are covered before the next paycheck arrives.

Sinking Fund Syncing

Monthly budget planning allocates funds based on regular income cycles, while paycheck budgeting distributes expenses immediately upon receipt of each paycheck; syncing these approaches with sinking funds ensures timely savings for irregular or future expenses without disrupting cash flow. Maintaining alignment between sinking fund contributions and paycheck deposits enhances financial stability and prevents overspending.

Micro-Budget Mapping

Micro-budget mapping enhances money management by breaking down monthly budgets into paycheck-specific allocations, allowing precise tracking of expenses and savings per pay period. This method improves cash flow control and reduces overspending by aligning spending limits directly with incoming paychecks.

Income-Driven Budget Splitting

Income-driven budget splitting allocates funds based on each paycheck, creating a dynamic monthly budget that adjusts to variable income streams for improved cash flow management. This method ensures essential expenses are prioritized immediately upon receiving paychecks, reducing the risk of overspending and enhancing financial stability.

Paycheck Frequency Adjustment

Adjusting your budget based on paycheck frequency improves cash flow management by aligning expenses with income intervals, preventing overspending between paychecks. Incorporating paycheck frequency adjustments ensures accurate allocation of funds for bills, savings, and discretionary spending within each pay period.

Expense Anchoring

Monthly budget frameworks provide a comprehensive overview of recurring expenses spread across the entire month, facilitating long-term financial planning. Paycheck budget models anchor expense allocations directly to individual income deposits, enhancing real-time cash flow management and preventing overspending between pay periods.

Real-Time Spend Tracking

Real-time spend tracking in monthly budgets allows consumers to monitor expenses continuously, preventing overspending before the month ends. Paycheck budgeting ties spending limits to each income deposit, enabling dynamic adjustments based on current financial inflows and reducing the risk of cash shortages.

Paycheck Allocation Automation

Paycheck allocation automation streamlines money management by directly dividing income into designated categories such as savings, bills, and discretionary spending immediately upon receipt, reducing the risk of overspending. This method offers more precise control compared to traditional monthly budgets by aligning expenses with each paycheck cycle, enhancing cash flow visibility and financial discipline.

Monthly budget vs Paycheck budget for money management. Infographic