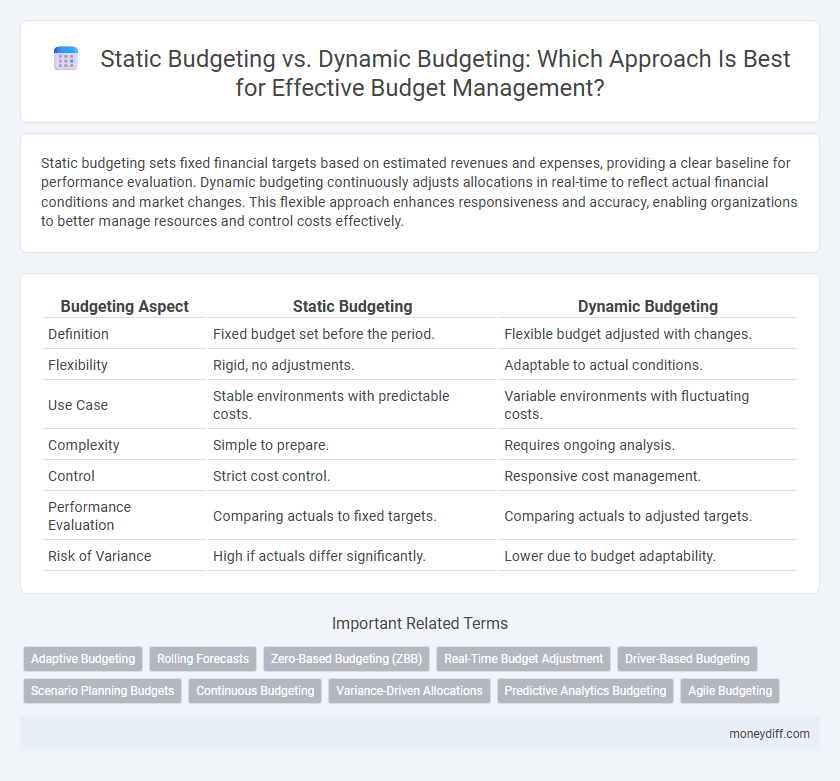

Static budgeting sets fixed financial targets based on estimated revenues and expenses, providing a clear baseline for performance evaluation. Dynamic budgeting continuously adjusts allocations in real-time to reflect actual financial conditions and market changes. This flexible approach enhances responsiveness and accuracy, enabling organizations to better manage resources and control costs effectively.

Table of Comparison

| Budgeting Aspect | Static Budgeting | Dynamic Budgeting |

|---|---|---|

| Definition | Fixed budget set before the period. | Flexible budget adjusted with changes. |

| Flexibility | Rigid, no adjustments. | Adaptable to actual conditions. |

| Use Case | Stable environments with predictable costs. | Variable environments with fluctuating costs. |

| Complexity | Simple to prepare. | Requires ongoing analysis. |

| Control | Strict cost control. | Responsive cost management. |

| Performance Evaluation | Comparing actuals to fixed targets. | Comparing actuals to adjusted targets. |

| Risk of Variance | High if actuals differ significantly. | Lower due to budget adaptability. |

Introduction to Static Budgeting and Dynamic Budgeting

Static budgeting establishes a fixed financial plan based on predetermined assumptions, maintaining consistent expense and revenue targets regardless of actual business performance. Dynamic budgeting adjusts projections continually to reflect real-time changes in operational conditions, enabling more accurate and flexible financial management. Understanding the distinction between these budgeting methods is essential for businesses aiming to align resources efficiently with changing market demands.

Key Differences Between Static and Dynamic Budgets

Static budgeting sets a fixed allocation of funds based on predetermined estimates, remaining unchanged regardless of actual business performance or market fluctuations. Dynamic budgeting continuously adjusts financial plans in response to real-time data, enabling more flexibility and responsiveness to changes in revenue, costs, or operational needs. Key differences include the adaptability of dynamic budgets to evolving conditions versus the fixed, rigid structure of static budgets, impacting decision-making accuracy and resource allocation efficiency.

Advantages of Static Budgeting

Static budgeting provides clear financial targets by establishing fixed expense and revenue limits, simplifying performance evaluation and variance analysis. It enhances cost control through predefined spending caps, enabling tighter management of resources in stable operational environments. This approach improves accountability by setting consistent benchmarks that departments can reliably follow throughout the fiscal period.

Limitations of Static Budgeting

Static budgeting often fails to accommodate changes in business conditions, leading to inaccuracies in financial planning and control. Its rigid structure makes it difficult to adjust for unexpected expenses or shifts in revenue, reducing its effectiveness in dynamic markets. As a result, static budgets can limit managerial flexibility and impede timely decision-making.

Benefits of Dynamic Budgeting

Dynamic budgeting offers enhanced flexibility by allowing real-time adjustments to reflect changes in market conditions and operational performance. It improves accuracy in forecasting by continuously incorporating actual financial data, which enables better resource allocation and cost control. This budgeting method supports proactive decision-making, promoting agility and responsiveness in managing financial risks and opportunities.

Drawbacks of Dynamic Budgeting

Dynamic budgeting often leads to increased complexity and time consumption due to constant adjustments in response to changing business conditions. Its reliance on frequent data updates can result in resource-intensive processes, potentially diverting focus from strategic planning. Moreover, the volatility in projections may cause decision-making challenges and reduced predictability compared to static budgeting.

When to Use a Static Budget

A static budget is most effective when organizations face predictable and stable operating conditions, allowing for fixed expense and revenue targets. It suits businesses with consistent sales volumes and minimal fluctuations in costs, such as government agencies or manufacturing firms with steady production levels. Employing a static budget provides clear financial expectations and simplifies variance analysis in these controlled environments.

When to Opt for a Dynamic Budget

Opt for a dynamic budget when operating in highly volatile markets or industries with frequent changes in demand, costs, or regulations, as it allows for continuous adjustments to reflect real-time financial performance and business conditions. Dynamic budgeting is ideal for startups, project-based businesses, and sectors like technology or retail, where flexibility and responsiveness to market trends are critical for maintaining profitability and competitive advantage. This approach enhances decision-making accuracy by incorporating up-to-date data, unlike static budgeting which relies on fixed assumptions and can lead to misaligned resource allocation during periods of uncertainty.

Impact on Financial Decision-Making

Static budgeting provides a fixed financial plan that facilitates straightforward variance analysis but may limit responsiveness to changing market conditions, potentially leading to suboptimal financial decisions. Dynamic budgeting adjusts forecasts and allocations based on real-time data, enhancing flexibility and accuracy in financial decision-making to better align resources with organizational goals. Effective financial management often integrates static and dynamic budgeting methods to balance stability with adaptability in response to economic fluctuations.

Choosing the Right Budgeting Method for Your Needs

Static budgeting provides a fixed financial plan based on initial assumptions, making it ideal for organizations with stable revenues and predictable expenses. Dynamic budgeting adjusts continuously to reflect actual performance and changing conditions, offering flexibility for businesses facing fluctuating markets or uncertain costs. Selecting between static and dynamic budgeting depends on the need for control versus adaptability in managing financial resources effectively.

Related Important Terms

Adaptive Budgeting

Adaptive budgeting, a form of dynamic budgeting, allows organizations to revise financial plans regularly based on real-time data and changing market conditions, enhancing flexibility and responsiveness. Unlike static budgeting, which sets fixed financial targets regardless of external shifts, adaptive budgeting improves accuracy and decision-making by continuously aligning budgets with current business environments.

Rolling Forecasts

Static budgeting sets fixed financial targets for a specific period, offering stability but limited adaptability to changing market conditions. Dynamic budgeting, often implemented through rolling forecasts, continuously updates projections based on real-time data, enhancing accuracy and enabling responsive resource allocation.

Zero-Based Budgeting (ZBB)

Static budgeting allocates fixed resources based on a predetermined plan regardless of actual activity levels, often leading to inefficiencies in dynamic environments. Zero-Based Budgeting (ZBB) enhances dynamic budgeting by requiring each expense to be justified from scratch, promoting resource optimization and adaptability to changing financial conditions.

Real-Time Budget Adjustment

Static budgeting sets fixed financial plans that remain unchanged throughout the period, offering stability but lacking flexibility for unexpected expenses or revenue changes. Dynamic budgeting enables real-time budget adjustments by continuously updating forecasts based on actual performance data, improving responsiveness and accuracy in financial management.

Driver-Based Budgeting

Driver-based budgeting leverages key business drivers such as sales volume, cost per unit, and market trends to create more responsive and flexible financial plans compared to static budgeting, which relies on fixed assumptions and predefined figures. This dynamic approach enables organizations to adjust budgets in real-time based on actual performance and changing conditions, enhancing accuracy, resource allocation, and strategic decision-making.

Scenario Planning Budgets

Static budgeting allocates fixed financial resources based on predetermined assumptions, providing a stable benchmark but lacking flexibility to adapt to changing business conditions. Dynamic budgeting incorporates scenario planning techniques to adjust budget forecasts continuously, enabling organizations to respond effectively to varying market uncertainties and optimize resource allocation.

Continuous Budgeting

Static budgeting establishes fixed financial plans based on predetermined assumptions, limiting flexibility in adapting to market changes, whereas dynamic budgeting, particularly continuous budgeting, involves regular updates and revisions to reflect real-time financial data and operational shifts. Continuous budgeting enhances accuracy and responsiveness by enabling organizations to recalibrate their budget forecasts monthly or quarterly, improving financial control and strategic decision-making.

Variance-Driven Allocations

Static budgeting sets fixed financial targets, limiting flexibility in addressing variances, whereas dynamic budgeting leverages real-time data to adjust allocations promptly, enhancing responsiveness to unexpected expenses or revenue shifts. Variance-driven allocations in dynamic budgets optimize resource distribution by reallocating funds based on actual performance variances, improving accuracy and financial control.

Predictive Analytics Budgeting

Static budgeting sets fixed financial targets based on historical data, limiting flexibility in response to market changes, whereas dynamic budgeting leverages predictive analytics to continuously adjust forecasts and resource allocations in real time. Predictive analytics budgeting enhances accuracy by analyzing trends, patterns, and external variables, enabling organizations to anticipate financial outcomes and optimize budget performance proactively.

Agile Budgeting

Static budgeting establishes fixed financial allocations based on initial projections, limiting flexibility during changing business conditions, while dynamic budgeting, often aligned with agile budgeting principles, allows continuous adjustments to reflect real-time financial performance and market fluctuations. Agile budgeting enhances responsiveness by integrating iterative planning and frequent reviews, enabling organizations to reallocate resources swiftly and optimize budget efficiency in rapidly evolving environments.

Static Budgeting vs Dynamic Budgeting for Budget Infographic