Budgeting involves setting predefined spending limits to control expenses and ensure savings, while reverse budgeting starts with setting savings goals first and allocating any remaining funds for spending. Reverse budgeting prioritizes long-term financial objectives, making it easier to build wealth and emergencies funds without feeling restricted. Choosing between the two depends on whether you prefer structured spending control or goal-focused financial planning.

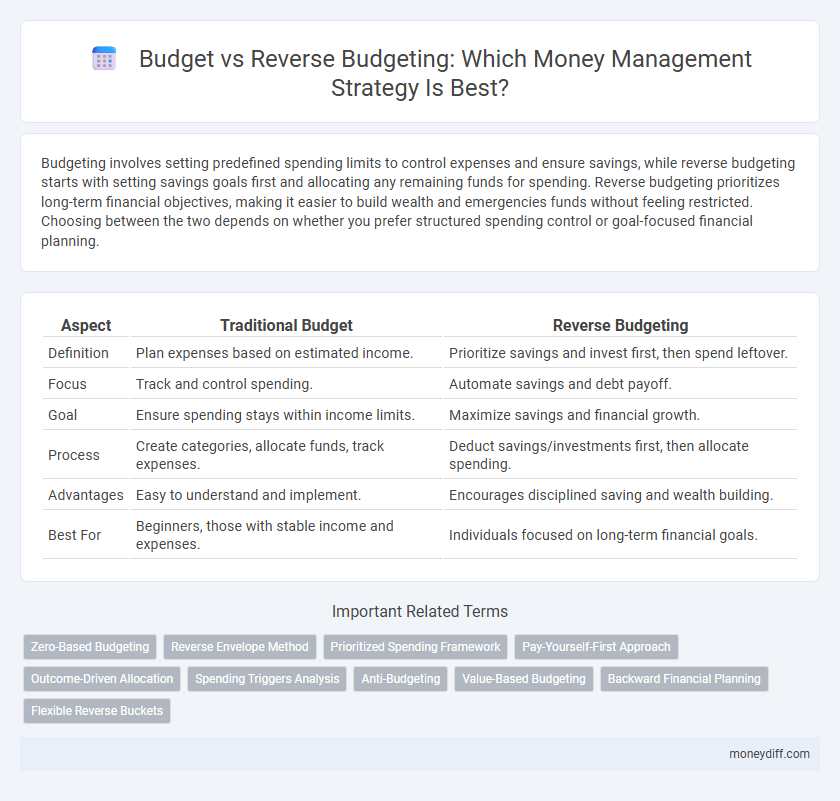

Table of Comparison

| Aspect | Traditional Budget | Reverse Budgeting |

|---|---|---|

| Definition | Plan expenses based on estimated income. | Prioritize savings and invest first, then spend leftover. |

| Focus | Track and control spending. | Automate savings and debt payoff. |

| Goal | Ensure spending stays within income limits. | Maximize savings and financial growth. |

| Process | Create categories, allocate funds, track expenses. | Deduct savings/investments first, then allocate spending. |

| Advantages | Easy to understand and implement. | Encourages disciplined saving and wealth building. |

| Best For | Beginners, those with stable income and expenses. | Individuals focused on long-term financial goals. |

Understanding Traditional Budgeting

Traditional budgeting involves setting predefined spending limits based on income and expenses to control financial resources efficiently. It emphasizes allocating funds to specific categories like housing, food, and entertainment before the spending period begins. This method provides a clear framework for tracking expenses and ensuring adherence to financial goals.

What Is Reverse Budgeting?

Reverse budgeting emphasizes tracking expenses after income allocation rather than planning every expense upfront, prioritizing savings and debt repayment first. This method allows individuals to allocate a fixed amount to savings automatically, then spend freely within the remaining balance, promoting financial discipline without rigid restrictions. Reverse budgeting is effective for those seeking flexibility while ensuring consistent saving and managing financial goals efficiently.

Key Differences Between Budget and Reverse Budgeting

Budget involves allocating specific amounts of income to fixed categories such as expenses, savings, and investments, whereas reverse budgeting prioritizes saving first by automatically setting aside a predetermined amount before managing expenses. The main difference lies in the sequencing; traditional budgeting focuses on controlling spending to meet goals, while reverse budgeting ensures savings goals are met upfront, encouraging disciplined financial habits. Reverse budgeting often results in more consistent savings rates and can simplify money management by placing savings as a financial priority before discretionary spending.

Pros and Cons of Traditional Budgeting

Traditional budgeting provides a structured approach to managing income and expenses by setting predefined limits for each category, promoting disciplined spending and clear financial goals. However, this method often lacks flexibility, making it challenging to adapt to unexpected expenses or fluctuating income, which can lead to frustration or budget abandonment. Moreover, strict adherence to traditional budgets may limit opportunities for spontaneous savings or investment adjustments, reducing overall financial agility.

Advantages of Reverse Budgeting

Reverse budgeting prioritizes saving and investing first by automatically allocating funds to these goals before covering expenses, ensuring financial discipline. This method reduces the risk of overspending by setting spending limits based on what remains after savings, promoting long-term wealth growth. It simplifies money management by emphasizing proactive wealth accumulation rather than reactive expense tracking.

Which Budgeting Method Suits Your Financial Goals?

Budgeting involves planning expenses based on income, while reverse budgeting prioritizes saving first and allocates leftover funds for spending. If your financial goals emphasize disciplined saving and wealth accumulation, reverse budgeting aligns better by automatically securing savings before expenses. For goals centered on detailed expense control and cash flow management, traditional budgeting offers granular tracking to optimize spending habits.

Step-by-Step Guide to Creating a Traditional Budget

Creating a traditional budget begins with tracking all sources of income and categorizing monthly expenses, including fixed costs like rent and variable costs such as groceries. Next, allocate specific spending limits for each category based on financial goals and past spending patterns to ensure control over cash flow. Regularly reviewing and adjusting the budget helps maintain financial discipline and accommodates changes in income or expenses.

How to Start with Reverse Budgeting

Reverse budgeting starts by prioritizing savings and essential expenses, ensuring money is allocated to goals before discretionary spending. Track income and fixed costs to determine the exact amount to save monthly, then adjust variable spending accordingly. This method promotes disciplined saving habits and clearer financial goals compared to traditional budgeting.

Common Mistakes in Both Budgeting Methods

Common mistakes in both traditional budgeting and reverse budgeting include underestimating expenses and failing to account for irregular costs, leading to inaccurate financial plans. Overly rigid spending limits often result in frustration and non-compliance, reducing the effectiveness of either method. Both approaches also commonly neglect the importance of regular review and adjustment, which is crucial for aligning budgets with changing financial goals and circumstances.

Choosing the Right Strategy for Effective Money Management

Budgeting involves allocating income to planned expenses, ensuring financial goals are met through disciplined spending, while reverse budgeting prioritizes savings by setting aside funds first before covering expenditures. Choosing the right strategy depends on individual financial behavior and goals; traditional budgeting suits structured planners, whereas reverse budgeting appeals to those who prefer saving proactively. Effective money management hinges on aligning the strategy with one's cash flow, spending habits, and long-term objectives to maximize financial stability.

Related Important Terms

Zero-Based Budgeting

Zero-Based Budgeting (ZBB) allocates every dollar of income to specific expenses, savings, or debt repayment, ensuring no funds are left unassigned and promoting precise money management. Unlike traditional budgeting, which adjusts prior budgets, ZBB starts from a "zero base" each period, enabling more accurate control over spending and resource allocation.

Reverse Envelope Method

The Reverse Envelope Method allocates funds to savings and essentials before discretionary spending, ensuring financial goals are met first and reducing the risk of overspending. Unlike traditional budgeting that assigns limits to expenses upfront, this approach prioritizes saving and debt repayment, promoting disciplined money management and improved financial stability.

Prioritized Spending Framework

Prioritized Spending Framework enhances money management by focusing on essential expenses first, creating a flexible approach unlike traditional budgeting that rigidly allocates funds. Reverse Budgeting allocates funds to savings and goals before spending, promoting financial discipline through prioritized cash flow management.

Pay-Yourself-First Approach

The Pay-Yourself-First approach prioritizes saving a predetermined portion of income before allocating funds to expenses, aligning closely with reverse budgeting by focusing on financial goals first rather than expense tracking. This method enhances money management by ensuring consistent savings contributions, promoting long-term financial stability and disciplined spending habits.

Outcome-Driven Allocation

Outcome-driven allocation in budgeting directs funds towards specific financial goals, enhancing control and efficiency by prioritizing spending based on expected results. Reverse budgeting flips traditional methods by first setting desired outcomes, then working backwards to allocate resources, ensuring every dollar aligns with targeted objectives.

Spending Triggers Analysis

Spending triggers analysis in budgeting identifies patterns and emotional drivers behind expenses, enabling precise control of cash flow and reduction of impulsive purchases. Reverse budgeting prioritizes savings by allocating funds first, then adjusting discretionary spending, allowing individuals to manage spending triggers with a proactive, goal-oriented approach.

Anti-Budgeting

Anti-budgeting, or reverse budgeting, prioritizes saving and investing first before allocating funds for expenses, promoting financial discipline and long-term wealth accumulation. This method contrasts with traditional budgeting by focusing on fixed saving goals, reducing the risk of overspending and fostering proactive money management.

Value-Based Budgeting

Value-Based Budgeting prioritizes expenses aligned with personal or organizational values, promoting mindful spending and long-term financial satisfaction. Unlike Reverse Budgeting, which sets savings goals first and budgets the remainder, Value-Based Budgeting ensures that every dollar spent enhances quality of life and contributes to meaningful objectives.

Backward Financial Planning

Backward financial planning, or reverse budgeting, prioritizes setting financial goals and determining the necessary savings to achieve them before allocating monthly expenses, unlike traditional budgeting which starts by tracking and limiting spending categories. This method enhances money management by ensuring that essential long-term objectives, such as retirement funds or debt repayment, guide daily financial decisions, promoting disciplined saving over discretionary spending.

Flexible Reverse Buckets

Flexible Reverse Buckets in reverse budgeting allocate money by prioritizing savings and expenses in adjustable categories, allowing for dynamic redistribution based on real-time financial goals and spending patterns. This method enhances money management by providing greater adaptability compared to traditional budgets, which often have fixed limits and less responsiveness to changing financial circumstances.

Budget vs Reverse Budgeting for money management. Infographic