Incremental budgeting allocates funds based on previous periods with adjustments for expected changes, offering simplicity and stability but may perpetuate inefficiencies. Rolling forecast budgeting continuously updates financial plans by incorporating real-time data and changing assumptions, enhancing agility and responsiveness to market dynamics. Choosing between these methods depends on an organization's need for flexibility versus predictability in budget management.

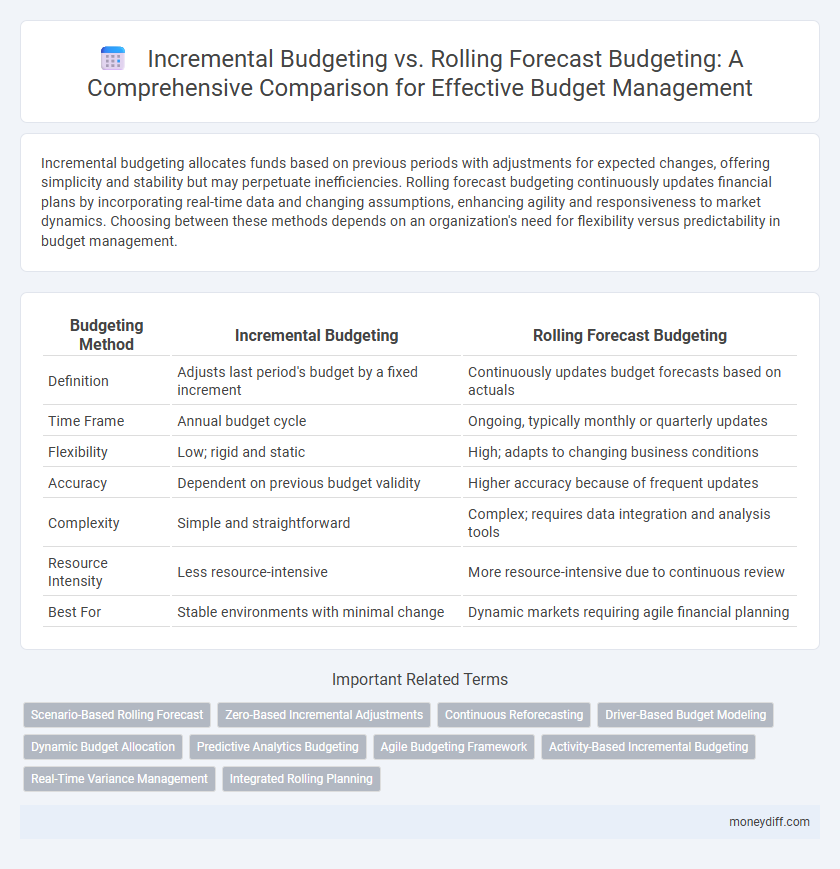

Table of Comparison

| Budgeting Method | Incremental Budgeting | Rolling Forecast Budgeting |

|---|---|---|

| Definition | Adjusts last period's budget by a fixed increment | Continuously updates budget forecasts based on actuals |

| Time Frame | Annual budget cycle | Ongoing, typically monthly or quarterly updates |

| Flexibility | Low; rigid and static | High; adapts to changing business conditions |

| Accuracy | Dependent on previous budget validity | Higher accuracy because of frequent updates |

| Complexity | Simple and straightforward | Complex; requires data integration and analysis tools |

| Resource Intensity | Less resource-intensive | More resource-intensive due to continuous review |

| Best For | Stable environments with minimal change | Dynamic markets requiring agile financial planning |

Introduction to Incremental Budgeting and Rolling Forecast Budgeting

Incremental budgeting allocates funds based on previous budgets, adjusting for expected changes, providing a straightforward and stable approach to budget planning. Rolling forecast budgeting continuously updates financial forecasts by incorporating real-time data, allowing for more dynamic and flexible budget management. Both methods serve distinct purposes, with incremental budgeting emphasizing predictability and rolling forecasts enhancing adaptability in financial planning.

Key Principles of Incremental Budgeting

Incremental budgeting allocates resources based on the previous period's budget, adjusting for small changes in revenue or expenses, emphasizing stability and simplicity in financial planning. This method assumes existing budgets are mostly efficient, promoting incremental increases or decreases aligned with historical data. Key principles include relying on past budgets as a baseline, minimal adjustments for growth or reduction, and ease of implementation.

Core Features of Rolling Forecast Budgeting

Rolling forecast budgeting continuously revises financial projections based on real-time data, allowing businesses to adapt quickly to market changes and improve accuracy over static incremental budgeting. It emphasizes ongoing adjustments to revenue, expenses, and cash flow forecasts, typically extending 12 to 18 months into the future. This dynamic approach enhances strategic decision-making by integrating updated assumptions and performance metrics regularly.

Comparison: Incremental Budgeting vs Rolling Forecast Budgeting

Incremental Budgeting adjusts previous budgets by a fixed percentage to set new allocations, making it straightforward but often less responsive to changing business conditions. Rolling Forecast Budgeting continuously updates budget projections based on real-time data and market trends, enhancing agility and accuracy in financial planning. While Incremental Budgeting offers simplicity and stability, Rolling Forecast Budgeting provides dynamic insights crucial for adaptive strategy development.

Advantages of Incremental Budgeting

Incremental budgeting simplifies the budgeting process by using the previous period's budget as a base, allowing for quick adjustments and straightforward resource allocation. It ensures budget stability and control by making incremental changes, reducing the likelihood of drastic fluctuations or errors. This method is particularly effective for organizations with stable operations and predictable expenses, enabling efficient financial planning and consistent performance tracking.

Benefits of Rolling Forecast Budgeting

Rolling forecast budgeting enhances financial agility by continuously updating projections based on real-time data, allowing organizations to adapt swiftly to market changes. This approach improves accuracy in resource allocation and reduces the risk of budget obsolescence compared to static incremental budgeting. Companies benefit from better strategic decision-making and more efficient capital management through the dynamic and forward-looking nature of rolling forecasts.

Limitations of Incremental Budgeting

Incremental budgeting often perpetuates inefficiencies by basing new budgets on previous periods without thoroughly analyzing current needs or market changes. This approach can lead to resource misallocation and limits flexibility in responding to dynamic business environments. Firms relying solely on incremental budgeting may struggle to adapt to rapid industry shifts and evolving financial goals.

Drawbacks of Rolling Forecast Budgeting

Rolling forecast budgeting can lead to excessive complexity and resource consumption due to continuous updates and constant data analysis. The frequent revisions may cause decision fatigue among managers, diminishing their ability to focus on strategic priorities. Moreover, this approach may reduce long-term financial stability as it emphasizes short-term adjustments over comprehensive annual planning.

Choosing the Right Budgeting Method for Your Organization

Incremental budgeting builds on previous budgets by adjusting for expected changes, making it suitable for stable organizations with predictable expenses. Rolling forecast budgeting continuously updates financial projections based on real-time data, providing flexibility for dynamic environments and rapid decision-making. Selecting the right budgeting method depends on your organization's stability, industry volatility, and need for adaptability in financial planning.

Best Practices for Effective Budget Implementation

Incremental budgeting emphasizes using the previous period's budget as a baseline, adjusting for predicted changes, which simplifies preparation but can perpetuate inefficiencies. Rolling forecast budgeting involves continuously updating budget projections based on real-time data, enabling agile resource allocation and improved financial accuracy. Best practices for effective budget implementation include aligning budgeting methods with organizational goals, incorporating frequent performance reviews, and fostering cross-department collaboration to ensure adaptability and accountability.

Related Important Terms

Scenario-Based Rolling Forecast

Scenario-based rolling forecast budgeting enhances incremental budgeting by continuously updating financial plans with real-time data, allowing organizations to adapt to changing market conditions and operational uncertainties. This dynamic approach improves forecast accuracy and supports strategic decision-making through multiple what-if scenarios, unlike static incremental budgets that rely on historical data with limited flexibility.

Zero-Based Incremental Adjustments

Incremental budgeting adjusts prior budgets by small, zero-based increments to reflect changes in costs and activity levels, offering simplicity but risking budgetary inertia. Rolling forecast budgeting continuously updates budget assumptions based on real-time data, providing dynamic flexibility while still incorporating zero-based incremental adjustments to fine-tune financial accuracy.

Continuous Reforecasting

Incremental budgeting relies on historical budget data with minor adjustments, limiting adaptability to changing financial conditions. Rolling forecast budgeting enables continuous reforecasting by regularly updating projections based on real-time performance and market trends, enhancing agility and accuracy in financial planning.

Driver-Based Budget Modeling

Incremental budgeting uses historical data as a base and adjusts for incremental changes, optimizing driver-based budget modeling by focusing on specific cost and revenue drivers for more accurate projections. Rolling forecast budgeting continuously updates financial plans based on real-time driver metrics, enhancing adaptability and precision in dynamic business environments.

Dynamic Budget Allocation

Incremental budgeting relies on adjusting previous budget figures by a fixed percentage, which limits agility and responsiveness in dynamic budget allocation. Rolling forecast budgeting continuously updates budget projections based on real-time data, enabling more flexible and accurate allocation of resources aligned with changing business priorities.

Predictive Analytics Budgeting

Incremental budgeting allocates future budgets based on past expenditures with fixed adjustments, limiting its ability to incorporate predictive analytics for dynamic forecasting. Rolling forecast budgeting leverages real-time data and predictive analytics, enabling continuous updates and more accurate financial planning aligned with changing market conditions.

Agile Budgeting Framework

Incremental budgeting allocates resources based on previous budgets with slight adjustments, making it less adaptable to rapid market changes compared to rolling forecast budgeting, which continuously updates financial plans using real-time data, enhancing responsiveness within an agile budgeting framework. Rolling forecast budgeting supports dynamic decision-making and aligns with agile methodology by promoting continuous monitoring and adjustment of budget allocations to optimize resource utilization and strategic goals.

Activity-Based Incremental Budgeting

Activity-Based Incremental Budgeting allocates funds based on detailed analysis of past activities, refining incremental budgeting by linking budget changes to specific operational drivers. This method contrasts with Rolling Forecast Budgeting, which continuously updates projections, as it emphasizes historical cost behavior and activity efficiency to optimize resource allocation.

Real-Time Variance Management

Incremental budgeting relies on historical data to create budgets based on previous periods, often causing delays in identifying variances and limiting real-time responsiveness. Rolling forecast budgeting updates projections continuously throughout the fiscal year, enabling dynamic variance management and more timely financial adjustments.

Integrated Rolling Planning

Incremental budgeting builds the new budget based on prior period figures with incremental adjustments, often limiting flexibility and responsiveness to change. Integrated rolling planning in rolling forecast budgeting continuously updates financial plans based on real-time data, improving accuracy and strategic alignment across multiple periods.

Incremental Budgeting vs Rolling Forecast Budgeting for Budget Infographic