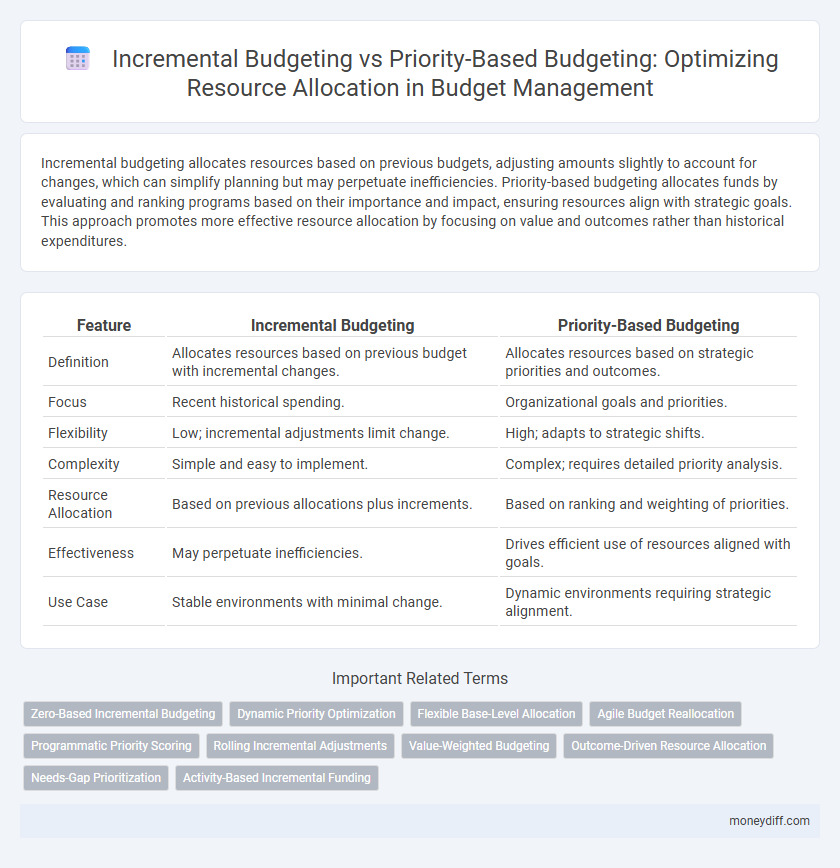

Incremental budgeting allocates resources based on previous budgets, adjusting amounts slightly to account for changes, which can simplify planning but may perpetuate inefficiencies. Priority-based budgeting allocates funds by evaluating and ranking programs based on their importance and impact, ensuring resources align with strategic goals. This approach promotes more effective resource allocation by focusing on value and outcomes rather than historical expenditures.

Table of Comparison

| Feature | Incremental Budgeting | Priority-Based Budgeting |

|---|---|---|

| Definition | Allocates resources based on previous budget with incremental changes. | Allocates resources based on strategic priorities and outcomes. |

| Focus | Recent historical spending. | Organizational goals and priorities. |

| Flexibility | Low; incremental adjustments limit change. | High; adapts to strategic shifts. |

| Complexity | Simple and easy to implement. | Complex; requires detailed priority analysis. |

| Resource Allocation | Based on previous allocations plus increments. | Based on ranking and weighting of priorities. |

| Effectiveness | May perpetuate inefficiencies. | Drives efficient use of resources aligned with goals. |

| Use Case | Stable environments with minimal change. | Dynamic environments requiring strategic alignment. |

Understanding Incremental Budgeting: Core Principles

Incremental budgeting focuses on adjusting the previous period's budget by a fixed increment, typically based on past expenditures and anticipated changes, which simplifies planning but may perpetuate inefficiencies. This method assumes that existing resource allocations are generally appropriate, making small adjustments to accommodate inflation, growth, or policy shifts without a complete overhaul. Incremental budgeting's core principle emphasizes stability and predictability in resource allocation but often limits strategic reallocation aligned with organizational priorities.

Defining Priority-Based Budgeting: An Overview

Priority-based budgeting allocates resources based on the importance and strategic value of programs rather than historical spending patterns. This method identifies key organizational goals and ranks initiatives to ensure funds are directed toward high-impact activities. Unlike incremental budgeting, it encourages efficiency by reassessing priorities annually, promoting alignment with evolving objectives.

Key Differences Between Incremental and Priority-Based Budgeting

Incremental budgeting allocates resources by adjusting previous budgets with incremental changes, often perpetuating historical spending patterns. Priority-based budgeting reallocates funds based on strategic objectives, focusing resources on high-impact programs aligned with organizational goals. The key difference lies in incremental budgeting's reliance on past expenditures versus priority-based budgeting's emphasis on evaluating and funding priorities to optimize resource utilization.

Pros and Cons of Incremental Budgeting

Incremental budgeting simplifies resource allocation by adjusting previous budgets with minor changes, promoting stability and ease of implementation. This method can lead to inefficient resource use, as it often perpetuates past spending patterns without considering current priorities or performance outcomes. Organizations using incremental budgeting may struggle to reallocate funds effectively when faced with shifting strategic goals or external changes.

Advantages and Challenges of Priority-Based Budgeting

Priority-Based Budgeting enhances resource allocation by aligning expenditures with organizational goals and maximizing the impact of limited funds. It promotes transparency and strategic decision-making by evaluating programs based on their contribution to priorities. Challenges include the complexity of defining accurate priorities and the potential resistance from stakeholders accustomed to traditional incremental methods.

Impact on Resource Allocation: Efficiency and Effectiveness

Incremental budgeting allocates resources based on previous budgets, often leading to inefficiencies by perpetuating past spending patterns without thorough evaluation. Priority-based budgeting enhances resource allocation efficiency by directing funds toward programs with the highest strategic impact and measurable outcomes. Organizations using priority-based methods typically experience improved effectiveness in achieving goals through alignment of resources with core priorities, optimizing overall budget performance.

Suitability for Different Organizational Structures

Incremental budgeting suits stable organizations with predictable expenses, enabling straightforward adjustments to prior budgets by adding or subtracting increments. Priority-based budgeting aligns better with dynamic or complex organizations, focusing on funding activities based on strategic importance and outcomes rather than historical spending. Organizations with decentralized or project-driven structures benefit from priority-based approaches for flexible, goal-oriented resource allocation.

Implementation Process: Step-by-Step Comparison

Incremental budgeting involves adjusting the previous year's budget by adding or subtracting a specific percentage, simplifying the implementation process with clear steps like reviewing past expenditures and applying incremental changes. Priority-based budgeting requires identifying key organizational goals, ranking programs by importance, and allocating resources accordingly, which demands a more detailed analysis and stakeholder involvement during implementation. The incremental approach is faster but less flexible, while priority-based budgeting offers strategic alignment at the cost of increased complexity in execution.

Real-World Case Studies: Incremental vs Priority-Based Approaches

Real-world case studies reveal that incremental budgeting often results in resource allocation based on historical expenditure patterns, which may perpetuate inefficiencies. Priority-based budgeting reallocates resources by evaluating program outcomes and aligning funds with strategic objectives, leading to more effective use of limited budgets. Organizations adopting priority-based approaches report improved transparency and better alignment with mission-critical priorities compared to incremental methods.

Choosing the Right Budgeting Method for Your Organization

Incremental budgeting allocates resources based on previous periods' budgets, promoting stability but risking inefficiency by perpetuating past spending patterns. Priority-based budgeting directs funds toward high-impact programs aligned with strategic goals, enhancing resource utilization and organizational effectiveness. Selecting the right method depends on organizational goals, financial flexibility, and the need for accountability in resource allocation.

Related Important Terms

Zero-Based Incremental Budgeting

Zero-Based Incremental Budgeting combines the systematic evaluation of every expense from a zero base with incremental adjustments, ensuring resource allocation aligns with current priorities and avoids unnecessary spending. This hybrid approach enhances financial efficiency by integrating detailed cost justification and adaptive budget increases based on organizational goals.

Dynamic Priority Optimization

Incremental budgeting allocates funds based on previous budgets with slight adjustments, often limiting adaptability in dynamic environments, while priority-based budgeting allocates resources by evaluating and ranking program impact and efficiency, enabling dynamic priority optimization that aligns spending with strategic goals and responsiveness to changing needs. Dynamic priority optimization enhances resource allocation by continuously reassessing priorities, ensuring budget decisions maximize value and responsiveness rather than merely adjusting historical expenditures.

Flexible Base-Level Allocation

Incremental budgeting allocates resources based on previous budgets with minor adjustments, limiting flexibility in base-level allocation and often perpetuating inefficiencies. Priority-based budgeting enhances resource allocation by focusing on funding programs aligned with organizational goals, allowing more adaptable and strategic adjustments to base-level expenditures.

Agile Budget Reallocation

Incremental budgeting allocates resources based on previous budgets with slight adjustments, limiting flexibility in dynamic environments, while priority-based budgeting reallocates funds according to strategic goals, enhancing agility in resource management. Agile budget reallocation supports adaptive decision-making by continuously aligning financial resources with evolving project priorities and organizational needs.

Programmatic Priority Scoring

Incremental budgeting adjusts previous budgets by small amounts, often overlooking shifts in organizational goals, whereas priority-based budgeting allocates resources based on programmatic priority scoring to maximize impact. Programmatic priority scoring uses specific criteria and weighted metrics to evaluate and rank programs, ensuring funds are directed toward initiatives with the highest strategic value and return on investment.

Rolling Incremental Adjustments

Rolling incremental adjustments in incremental budgeting enable continuous, small-scale modifications based on prior budget cycles, promoting stability but potentially perpetuating inefficiencies. Priority-based budgeting reallocates resources by evaluating program importance and performance, driving strategic alignment and enhanced resource utilization.

Value-Weighted Budgeting

Value-weighted budgeting outperforms incremental budgeting by allocating resources based on quantified value contributions rather than historical expenditures, ensuring efficient prioritization aligned with organizational goals. This approach refines priority-based budgeting by integrating data-driven value assessments to optimize resource distribution and maximize return on investment.

Outcome-Driven Resource Allocation

Incremental budgeting allocates resources based on previous expenditures with minor adjustments, often maintaining existing priorities regardless of changing outcomes or strategic goals. Priority-based budgeting emphasizes outcome-driven resource allocation by aligning funding with organizational objectives and highest-impact programs, ensuring resources are directed toward initiatives that deliver measurable results and value.

Needs-Gap Prioritization

Incremental budgeting allocates resources based on previous budgets, often overlooking emerging needs and resulting in less flexibility. Priority-based budgeting uses needs-gap prioritization to align funds with organizational goals by systematically identifying and addressing resource shortfalls.

Activity-Based Incremental Funding

Activity-Based Incremental Funding in incremental budgeting allocates resources based on previous activity levels, ensuring stability and continuity while minimizing drastic changes in department expenditures. Priority-Based Budgeting, by contrast, allocates funds according to strategic priorities and outcomes, potentially leading to more efficient resource use but requiring comprehensive evaluation and realignment of existing activities.

Incremental Budgeting vs Priority-Based Budgeting for resource allocation. Infographic