Budgeting for money management involves tracking income and expenses to maintain financial stability, while a FIRE budget specifically targets aggressive saving and investing to achieve financial independence and early retirement. A traditional budget prioritizes balanced spending and saving habits, whereas a FIRE budget emphasizes maximizing savings rate and minimizing discretionary costs to accelerate wealth accumulation. Both approaches require disciplined planning, but the FIRE budget demands more stringent control to reach financial goals faster.

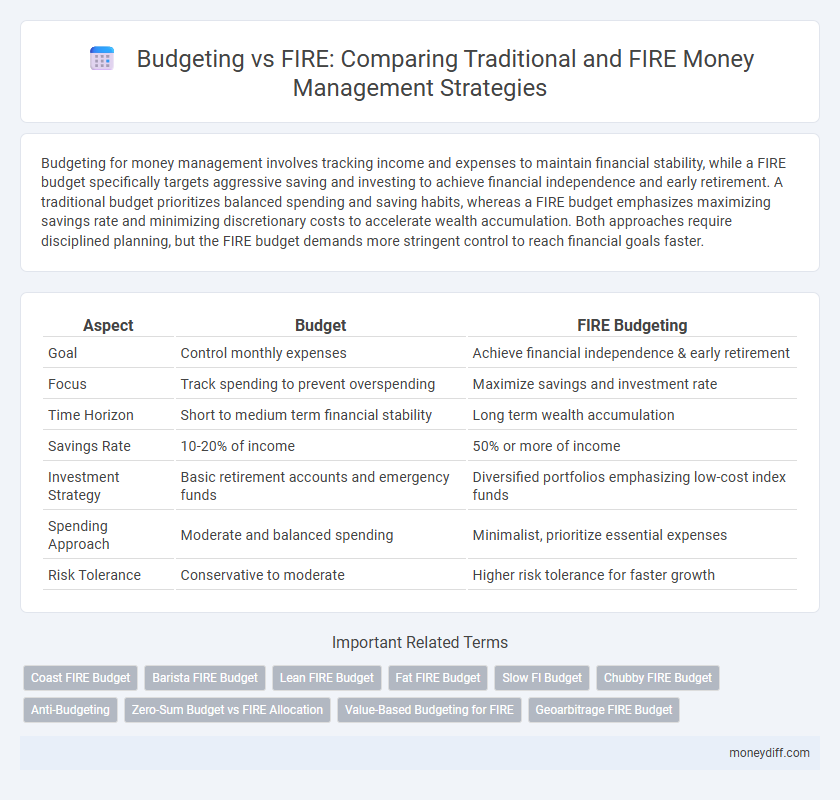

Table of Comparison

| Aspect | Budget | FIRE Budgeting |

|---|---|---|

| Goal | Control monthly expenses | Achieve financial independence & early retirement |

| Focus | Track spending to prevent overspending | Maximize savings and investment rate |

| Time Horizon | Short to medium term financial stability | Long term wealth accumulation |

| Savings Rate | 10-20% of income | 50% or more of income |

| Investment Strategy | Basic retirement accounts and emergency funds | Diversified portfolios emphasizing low-cost index funds |

| Spending Approach | Moderate and balanced spending | Minimalist, prioritize essential expenses |

| Risk Tolerance | Conservative to moderate | Higher risk tolerance for faster growth |

Understanding Traditional Budgeting Methods

Traditional budgeting methods involve allocating income to various expense categories based on past spending patterns and anticipated costs, emphasizing control and discipline. This approach relies on fixed monthly limits for essentials like housing, utilities, food, and discretionary spending, promoting financial stability through consistent monitoring. While effective for managing cash flow, traditional budgets often lack flexibility compared to FIRE (Financial Independence, Retire Early) budgeting, which prioritizes aggressive savings and investment goals to achieve early retirement.

What Is FIRE (Financial Independence, Retire Early) Budgeting?

FIRE (Financial Independence, Retire Early) budgeting emphasizes aggressive saving and investing strategies to achieve early retirement by significantly reducing expenses and maximizing income streams. Unlike traditional budgeting, which balances income with expenses for financial stability, FIRE budgeting prioritizes financial independence through high savings rates often exceeding 50%. This approach requires detailed tracking of net worth, passive income, and careful allocation of funds to optimize long-term wealth accumulation.

Key Differences Between Standard and FIRE Budgets

Standard budgets typically allocate income across fixed expenses, savings, and discretionary spending to maintain financial stability over time. FIRE (Financial Independence, Retire Early) budgets prioritize aggressive savings rates often exceeding 50%, minimizing discretionary expenses to accelerate wealth accumulation. Key differences include the FIRE budget's focus on early retirement goals and strict expense tracking versus the standard budget's balanced lifestyle approach.

Setting Financial Goals: Traditional vs. FIRE Approaches

Setting financial goals under traditional budgeting often emphasizes balancing daily expenses and long-term savings with a focus on steady income and moderate lifestyle adjustments. The FIRE (Financial Independence, Retire Early) budgeting approach prioritizes aggressive savings rates and investment strategies to achieve early retirement and financial autonomy. This shift requires detailed planning, disciplined spending, and a clear timeline for accumulating assets beyond conventional retirement age targets.

Income Allocation Strategies for Each Budgeting Style

Traditional budgeting allocates income by categorizing expenses into fixed, variable, and discretionary spending, focusing on balancing income and expenses to avoid debt. FIRE (Financial Independence, Retire Early) budgeting prioritizes aggressive savings and investment, often directing 50-70% of income towards retirement funds and reducing lifestyle expenses significantly. Income allocation in FIRE budgeting emphasizes accelerating asset growth through high savings rates and passive income generation to achieve early financial independence.

Expense Tracking: Minimizing vs. Optimizing Spending

Traditional budgeting emphasizes minimizing expenses by setting strict limits to reduce overall spending, often leading to financial discipline through careful expense tracking. FIRE budgeting focuses on optimizing spending by allocating resources toward meaningful goals and efficiently managing necessary expenses to maximize financial independence. Both methods rely on precise expense tracking but differ in intent: one aims to cut costs, while the other prioritizes strategic spending for long-term wealth building.

Savings Rates: Conventional Budgeting vs. FIRE Mindset

Conventional budgeting typically targets a modest savings rate of 10-20%, prioritizing balanced spending and financial stability. FIRE (Financial Independence, Retire Early) budgeting emphasizes aggressive savings rates often exceeding 50%, accelerating wealth accumulation for early retirement. Higher savings rates in FIRE budgeting significantly reduce time to financial independence by maximizing investment potential and compounding growth.

Investment Plans: Long-Term Wealth vs. Early Retirement

Budgeting for long-term wealth emphasizes consistent investment plans such as diversified portfolios, retirement accounts, and compound interest growth over decades. FIRE budgeting prioritizes aggressive savings rate and investments primarily aimed at achieving financial independence for early retirement, often utilizing tax-advantaged accounts and low-cost index funds. Both strategies require disciplined tracking but differ fundamentally in time horizons and liquidity needs for retirement funding.

Risk Management in Traditional and FIRE Budgeting

Traditional budgeting emphasizes cautious allocation to avoid overspending and safeguard against unexpected expenses, focusing on maintaining consistent cash flow and emergency funds. FIRE budgeting prioritizes aggressive savings and investment strategies to achieve financial independence rapidly, which entails higher risks due to market volatility and reduced short-term liquidity. Effective risk management in traditional budgets relies on conservative spending patterns, while FIRE budgeting requires continuous portfolio assessment and contingency planning to mitigate financial uncertainty.

Choosing the Right Budgeting Strategy for Your Lifestyle

Selecting the right budgeting strategy depends on personal financial goals and lifestyle preferences. Traditional budgeting allocates income to expenses and savings, offering flexibility for varying priorities, while FIRE budgeting emphasizes aggressive saving and investing to achieve early financial independence. Evaluating income stability, spending habits, and long-term objectives ensures the chosen approach maximizes financial control and aligns with individual aspirations.

Related Important Terms

Coast FIRE Budget

A Coast FIRE budget emphasizes saving aggressively early to allow investments to grow passively, minimizing the need for tight budgeting later, unlike traditional budgets which focus on controlling daily expenses. This strategy prioritizes reaching a financial threshold that covers future retirement without additional contributions, leveraging compound interest and long-term investment growth.

Barista FIRE Budget

Barista FIRE Budget emphasizes a hybrid approach where part-time work covers essential expenses while investments support financial independence, contrasting traditional strict Budget methods that focus solely on expense tracking and reduction. This strategy optimizes cash flow by balancing income streams and maintaining flexible spending aligned with long-term investment growth goals.

Lean FIRE Budget

A Lean FIRE budget emphasizes minimal essential expenses to achieve financial independence with a lower savings goal and reduced lifestyle costs, contrasting with traditional budgeting that allows for more discretionary spending. This method accelerates early retirement by focusing on frugality, essential living, and strategic cost-cutting, optimizing resource allocation for sustained financial freedom.

Fat FIRE Budget

Fat FIRE budgeting emphasizes maintaining a high standard of living through aggressive savings and investments, targeting early retirement with substantial disposable income. Unlike traditional budgeting, Fat FIRE budgeting allocates resources toward luxury expenses and greater financial freedom, ensuring a comfortable and affluent retirement lifestyle.

Slow FI Budget

Slow FI budgeting emphasizes deliberate, sustainable saving habits and prioritizes long-term financial independence over rapid wealth accumulation, contrasting with traditional budgeting that often targets short-term spending control. This approach integrates flexible expense tracking with mindful allocation to foster steady growth, reducing stress and enhancing financial resilience.

Chubby FIRE Budget

Chubby FIRE Budget emphasizes a higher annual spending target compared to traditional Budget methods, allowing for a more comfortable lifestyle during early retirement by accounting for inflation and lifestyle inflation. This approach balances aggressive savings with realistic expense projections, optimizing money management for sustained financial independence.

Anti-Budgeting

Anti-budgeting simplifies money management by prioritizing spending freedom over rigid tracking, contrasting sharply with traditional budgets and FIRE (Financial Independence, Retire Early) strategies that emphasize strict expense control and aggressive savings. This approach enhances financial flexibility by focusing on overall financial goals instead of detailed line-item monitoring, appealing to those seeking a less restrictive yet effective money management method.

Zero-Sum Budget vs FIRE Allocation

Zero-sum budgeting allocates every dollar of income to specific expenses, savings, or debt repayment, ensuring a balanced budget with no money left unassigned. In contrast, FIRE (Financial Independence, Retire Early) budgeting prioritizes aggressive savings and investments, often allocating a higher percentage of income toward retirement funds to achieve early financial independence.

Value-Based Budgeting for FIRE

Value-Based Budgeting for FIRE prioritizes allocating funds towards expenses that align with personal values and long-term financial independence goals, contrasting with traditional budgeting that emphasizes rigid spending categories. This approach enhances money management by focusing on maximizing financial freedom and intentional spending rather than simply limiting expenses.

Geoarbitrage FIRE Budget

Geoarbitrage FIRE budgeting leverages geographic cost-of-living differences to optimize retirement funds by focusing expenses in lower-cost areas while maintaining income from higher-paying regions. This strategy enhances financial independence by reducing the required FIRE budget compared to traditional budgeting that often overlooks regional economic disparities.

Budget vs FIRE Budgeting for money management. Infographic