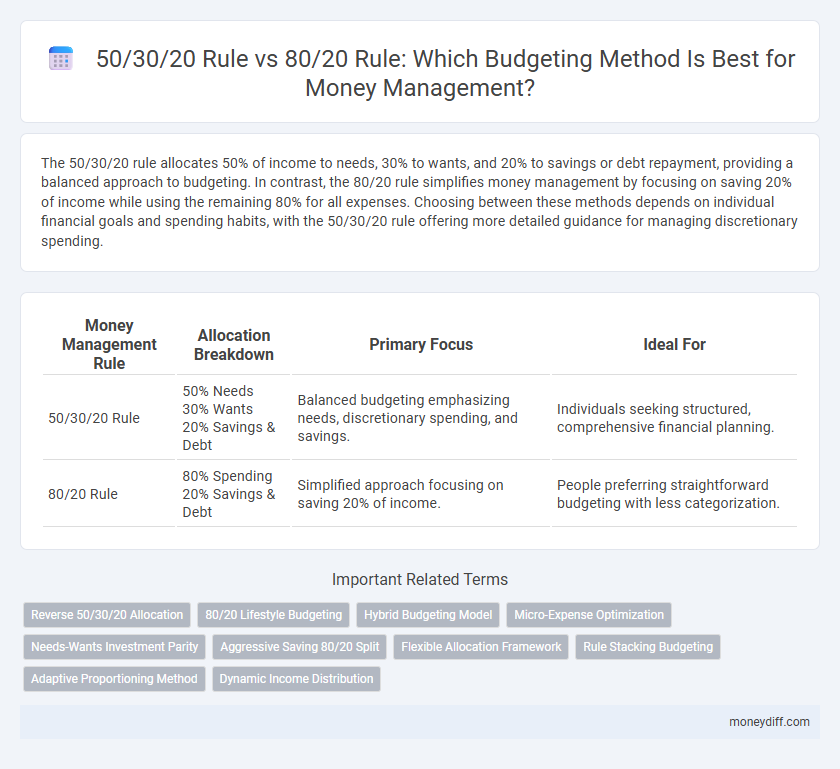

The 50/30/20 rule allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, providing a balanced approach to budgeting. In contrast, the 80/20 rule simplifies money management by focusing on saving 20% of income while using the remaining 80% for all expenses. Choosing between these methods depends on individual financial goals and spending habits, with the 50/30/20 rule offering more detailed guidance for managing discretionary spending.

Table of Comparison

| Money Management Rule | Allocation Breakdown | Primary Focus | Ideal For |

|---|---|---|---|

| 50/30/20 Rule |

50% Needs 30% Wants 20% Savings & Debt |

Balanced budgeting emphasizing needs, discretionary spending, and savings. | Individuals seeking structured, comprehensive financial planning. |

| 80/20 Rule |

80% Spending 20% Savings & Debt |

Simplified approach focusing on saving 20% of income. | People preferring straightforward budgeting with less categorization. |

Understanding the 50/30/20 Rule

The 50/30/20 rule divides after-tax income into three categories: 50% for needs, 30% for wants, and 20% for savings or debt repayment, offering a balanced framework for budgeting. This approach emphasizes prioritizing essential expenses while allowing flexibility for discretionary spending and financial goals. Understanding this rule helps individuals maintain financial discipline and effectively allocate their income for both present needs and future security.

What is the 80/20 Rule in Money Management?

The 80/20 Rule in money management focuses on allocating 80% of income toward essential expenses and lifestyle needs, while directing 20% toward savings and debt repayment. This rule emphasizes simplicity and flexibility, allowing individuals to manage finances without strict budgeting categories. It contrasts with the 50/30/20 Rule by offering a more streamlined approach to spending and saving priorities.

Key Differences between 50/30/20 and 80/20 Rules

The 50/30/20 rule divides income into 50% needs, 30% wants, and 20% savings or debt repayment, promoting a balanced allocation between essentials, discretionary spending, and financial goals. The 80/20 rule simplifies budgeting by allocating 80% of income for expenses and 20% strictly for savings or debt reduction, emphasizing aggressive saving habits. Key differences lie in spending flexibility and financial discipline, with the 50/30/20 rule offering more detailed categorization and spending control, while the 80/20 rule focuses primarily on maximizing savings with less granular expense divisions.

Pros and Cons of the 50/30/20 Budgeting Method

The 50/30/20 budgeting method allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, offering clear guidelines for balanced financial management. Its pros include simplicity, flexibility, and promoting savings while allowing discretionary spending, making it accessible for many income levels. However, the rigid percentage splits may not suit all financial situations, especially for those with high fixed expenses or irregular income, potentially limiting its effectiveness compared to the more savings-focused 80/20 rule.

Advantages and Disadvantages of the 80/20 Approach

The 80/20 Rule for money management simplifies budgeting by allocating 80% of income towards expenses and 20% towards savings or debt repayment, making it easier to implement and follow. Its advantages include less complexity and more flexibility compared to the 50/30/20 Rule, which divides income into three categories, potentially overwhelming some users. However, the 80/20 Rule may not provide detailed guidance on discretionary spending, risking overspending in non-essential areas and insufficient savings for long-term financial goals.

Which Rule Suits Your Financial Goals?

The 50/30/20 rule allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, offering a balanced approach for individuals aiming for steady financial growth and flexibility. The 80/20 rule emphasizes saving 20% of income while allowing 80% for expenses, which suits those prioritizing aggressive savings or debt payoff. Choosing the right rule depends on your financial goals, lifestyle, and discipline in managing discretionary spending.

Practical Examples: Applying Each Rule

The 50/30/20 rule allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, ideal for balanced financial planning with practical examples like budgeting $3,000 monthly into $1,500 for rent and bills, $900 for dining out and entertainment, and $600 toward savings. The 80/20 rule simplifies money management by dedicating 80% of income to expenses and 20% to savings, suitable for those seeking straightforward budgeting, demonstrated by allocating $2,400 for living costs and $600 for savings from a $3,000 income. Choosing between these rules depends on income stability, spending habits, and financial goals, ensuring tailored money management strategies that enhance budget adherence and financial health.

Tips for Switching Between Budgeting Methods

Switching between the 50/30/20 rule and the 80/20 rule requires clear tracking of expenses and income to recalibrate spending categories effectively. Focus on gradually adjusting discretionary spending within the flexible categories while maintaining mandatory savings targets to ensure financial stability. Utilize budgeting apps or spreadsheets to compare the outcomes of each rule and identify which aligns best with your financial goals and lifestyle.

Common Mistakes with the 50/30/20 and 80/20 Rules

Common mistakes with the 50/30/20 rule include misclassifying essentials and wants, leading to overspending in discretionary categories, while the 80/20 rule often results in insufficient budgeting for savings and unexpected expenses. Both rules can fail when applied rigidly without considering individual income variability and financial goals. Neglecting to adjust budget percentages for debt repayment or investment opportunities decreases their effectiveness in achieving financial stability.

Expert Recommendations: Choosing the Best Rule for You

Experts recommend evaluating personal financial goals and spending habits when choosing between the 50/30/20 and 80/20 budgeting rules. The 50/30/20 rule allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, offering balanced flexibility for most users. The 80/20 rule, focusing on saving 20% and spending 80% on all expenses, suits individuals prioritizing simplicity and aggressive savings goals.

Related Important Terms

Reverse 50/30/20 Allocation

The Reverse 50/30/20 allocation prioritizes saving 50% of income, allocating 30% to needs, and 20% to wants, contrasting traditional models by emphasizing aggressive savings for financial security. This approach restructures budget categories to enhance long-term wealth accumulation while still covering essential expenses and discretionary spending.

80/20 Lifestyle Budgeting

The 80/20 lifestyle budgeting method allocates 80% of income to spend freely while saving or investing 20%, promoting financial freedom without strict categorization. This approach simplifies money management by emphasizing flexibility and prioritizing long-term wealth building over rigid expense tracking inherent in the 50/30/20 rule.

Hybrid Budgeting Model

The Hybrid Budgeting Model combines the 50/30/20 Rule's balanced approach of allocating 50% to needs, 30% to wants, and 20% to savings with the 80/20 Rule's simplicity of saving 20% of income and spending 80%, optimizing flexibility and financial discipline. By merging structured spending categories with straightforward saving targets, this model enhances personalized money management efficiency and long-term financial stability.

Micro-Expense Optimization

The 50/30/20 Rule allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, optimizing micro-expenses by categorizing discretionary spending for better control. The 80/20 Rule directs 80% of income toward necessities and 20% to savings or debt, emphasizing strict prioritization and minimizing micro-expenses to maximize financial efficiency.

Needs-Wants Investment Parity

The 50/30/20 Rule allocates 50% of income to needs, 30% to wants, and 20% to investments, promoting a balanced approach to financial goals and lifestyle choices. In contrast, the 80/20 Rule designates 80% of income for expenses, combining needs and wants, and only 20% for investments, which may limit detailed budgeting between necessities and discretionary spending.

Aggressive Saving 80/20 Split

The aggressive saving 80/20 rule allocates 80% of income to necessities and savings while limiting discretionary spending to 20%, optimizing rapid wealth accumulation and financial security. This method contrasts with the 50/30/20 rule by emphasizing stricter budget discipline, prioritizing savings for aggressive financial goals and reducing lifestyle inflation.

Flexible Allocation Framework

The 50/30/20 Rule allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, providing a structured yet adaptable budget for diverse financial goals. The 80/20 Rule simplifies this by dedicating 80% to spending and 20% to savings, offering a flexible allocation framework that emphasizes saving consistency while allowing discretionary spending freedom.

Rule Stacking Budgeting

The 50/30/20 Rule allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, providing a balanced framework for managing finances. Rule Stacking Budgeting combines this with the 80/20 Rule, which reserves 80% for expenses and 20% for savings, enabling optimized cash flow management through layered budget strategies.

Adaptive Proportioning Method

The Adaptive Proportioning Method refines traditional budgeting by dynamically allocating income based on fluctuating financial goals and priorities rather than fixed percentages like the 50/30/20 or 80/20 rules. This flexible strategy enhances money management by adjusting spending, saving, and investing proportions to better align with an individual's evolving financial situation and objectives.

Dynamic Income Distribution

The 50/30/20 rule allocates 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, providing a balanced framework for dynamic income distribution. In contrast, the 80/20 rule simplifies budgeting by directing 80% of income to expenses and 20% to savings, ideal for those seeking a streamlined approach to managing fluctuating earnings.

50/30/20 Rule vs 80/20 Rule for money management. Infographic