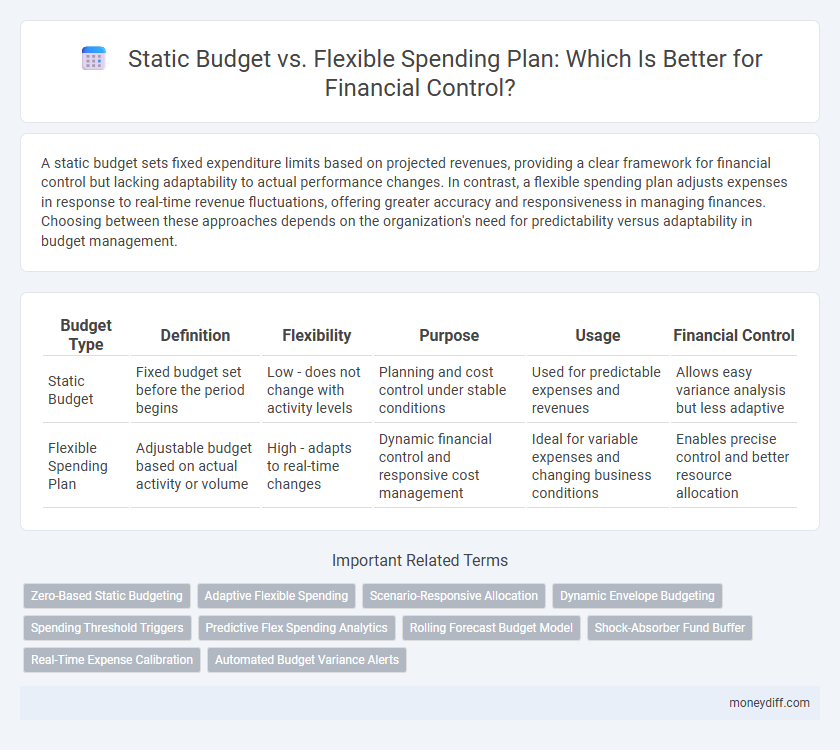

A static budget sets fixed expenditure limits based on projected revenues, providing a clear framework for financial control but lacking adaptability to actual performance changes. In contrast, a flexible spending plan adjusts expenses in response to real-time revenue fluctuations, offering greater accuracy and responsiveness in managing finances. Choosing between these approaches depends on the organization's need for predictability versus adaptability in budget management.

Table of Comparison

| Budget Type | Definition | Flexibility | Purpose | Usage | Financial Control |

|---|---|---|---|---|---|

| Static Budget | Fixed budget set before the period begins | Low - does not change with activity levels | Planning and cost control under stable conditions | Used for predictable expenses and revenues | Allows easy variance analysis but less adaptive |

| Flexible Spending Plan | Adjustable budget based on actual activity or volume | High - adapts to real-time changes | Dynamic financial control and responsive cost management | Ideal for variable expenses and changing business conditions | Enables precise control and better resource allocation |

Understanding Static Budgets: Definition and Purpose

Static budgets allocate fixed financial resources based on predetermined activity levels, providing a clear framework for cost control and performance evaluation. Their primary purpose is to set expenditure limits that remain constant regardless of actual operational volume, enabling straightforward comparison between planned and actual spending. This approach aids management in maintaining solid financial discipline but may lack responsiveness to fluctuating business conditions.

What Is a Flexible Spending Plan?

A flexible spending plan (FSP) allows organizations to adjust budget allocations based on actual revenue and expenses, providing dynamic financial control compared to a static budget. It helps managers respond to changing business conditions by modifying spending limits to optimize resource use and maintain financial stability. This adaptability enhances accuracy in forecasting and ensures better alignment with operational needs.

Key Differences Between Static and Flexible Budgets

Static budgets are fixed financial plans set before the fiscal period, offering limited adaptability to changes in actual business activity levels. Flexible budgets adjust dynamically based on real-time operational metrics such as sales volume or production output, allowing for more accurate expense management. Key differences include the static budget's reliance on predetermined figures versus the flexible budget's capacity to accommodate fluctuations and provide a realistic basis for performance evaluation.

Advantages of Using a Static Budget

A static budget provides clear financial targets by setting fixed spending limits based on predetermined revenue estimates, ensuring strict cost control and accountability. This approach simplifies performance evaluation by enabling straightforward comparisons between actual and budgeted figures, which helps identify variances and areas for cost reduction. Static budgets are particularly advantageous for organizations with stable revenue streams and predictable expenses, offering consistency in financial planning and resource allocation.

Benefits of Adopting a Flexible Spending Plan

A flexible spending plan enhances financial control by allowing real-time adjustments to budget allocations based on actual performance and changing business conditions, thereby reducing variance errors common in static budgets. It improves resource allocation efficiency by accommodating fluctuations in revenue and expenses, resulting in more accurate cash flow management and operational agility. Organizations adopting flexible spending plans benefit from increased responsiveness, better cost control, and improved strategic decision-making under dynamic market environments.

Limitations of Static Budgets for Financial Control

Static budgets often fail to account for fluctuations in actual revenue and expenses, limiting their effectiveness for precise financial control. They lack adaptability to changing market conditions, which can lead to budget variances and misaligned resource allocation. This rigidity can hinder proactive decision-making and responsiveness to unforeseen financial challenges.

Challenges of Implementing Flexible Spending Plans

Implementing flexible spending plans presents challenges such as accurately forecasting expenses due to variable cost behaviors and employee participation rates, complicating budget alignment. Organizations may face difficulties in maintaining financial control when actual spending fluctuates unpredictably, making it harder to measure performance against set targets. Moreover, administrative complexities and the need for continuous monitoring increase operational costs and require advanced financial management systems to ensure compliance and efficiency.

How to Choose the Right Budgeting Method for You

Choosing the right budgeting method depends on your business's predictability and adaptability needs; a static budget provides fixed financial targets ideal for stable environments, while a flexible spending plan adjusts based on actual performance, offering greater responsiveness to market fluctuations. Consider factors such as variability in costs, sales volume, and operational changes to determine which approach aligns with your financial control goals. Evaluating your organization's capacity to monitor and analyze real-time data ensures effective budget management and resource allocation.

Tips for Transitioning From Static to Flexible Budgeting

Transitioning from a static budget to a flexible spending plan requires accurate historical data analysis to forecast variable expenses effectively. Incorporate real-time monitoring tools and adjust budget allocations based on actual performance to enhance financial control. Engage key stakeholders in training sessions to ensure clear understanding and seamless adoption of the dynamic budgeting process.

Maximizing Financial Control Through Smart Budget Selection

Static budgets provide fixed financial allocations based on anticipated revenues, offering simplicity but limited adaptability to actual spending variations. Flexible spending plans adjust budget allocations dynamically according to real-time financial performance, enhancing responsiveness and precision in expenditure management. Choosing a flexible budget over a static one maximizes financial control by aligning spending closely with current business conditions, reducing the risk of overspending or underutilization.

Related Important Terms

Zero-Based Static Budgeting

Zero-based static budgeting requires each expense to be justified from scratch, ensuring strict allocation of resources without carrying over previous budgets. This method enhances financial control by eliminating unnecessary expenditures, unlike flexible spending plans that adjust based on activity levels and may permit budget variances.

Adaptive Flexible Spending

Adaptive flexible spending plans enable businesses to adjust budget allocations in real-time based on actual performance data, improving financial control and resource optimization. Unlike static budgets, which remain fixed regardless of changing conditions, flexible plans enhance responsiveness and support dynamic decision-making in volatile markets.

Scenario-Responsive Allocation

Static budget allocates fixed financial resources regardless of actual activity levels, limiting responsiveness to changing scenarios, while a flexible spending plan adjusts expenditures based on real-time operational demands and performance metrics. Scenario-responsive allocation enhances financial control by enabling dynamic budget modifications that align resource distribution with fluctuating business conditions and strategic priorities.

Dynamic Envelope Budgeting

Dynamic Envelope Budgeting offers precise financial control by adjusting spending limits within predefined categories based on actual income variations, contrasting with static budgets that remain fixed regardless of financial fluctuations. This flexible approach enhances budget accuracy and responsiveness, facilitating better management of resources in real-time financial scenarios.

Spending Threshold Triggers

Static budgets establish fixed spending limits regardless of actual activity levels, potentially leading to inefficiencies when unexpected expenses arise. Flexible spending plans incorporate spending threshold triggers that automatically adjust budgets based on real-time financial data, enhancing responsiveness and control in financial management.

Predictive Flex Spending Analytics

Predictive Flex Spending Analytics enhances financial control by dynamically adjusting budget allocations based on real-time spending patterns, unlike static budgets that remain fixed regardless of actual expenses. This approach enables more accurate forecasting and resource optimization, improving adaptability and minimizing variances in financial performance.

Rolling Forecast Budget Model

The Rolling Forecast Budget Model enhances financial control by continuously updating the static budget with real-time data, allowing for dynamic adjustments that reflect actual performance and market conditions. This approach outperforms traditional flexible spending plans by integrating forward-looking projections, improving accuracy in resource allocation and strategic decision-making.

Shock-Absorber Fund Buffer

A static budget sets fixed spending limits without adjusting for actual revenue fluctuations, while a flexible spending plan incorporates variable expenses tied to real-time income, enhancing financial adaptability. Incorporating a shock-absorber fund buffer within a flexible plan provides a crucial financial cushion to absorb unexpected costs, improving organizational resilience and control.

Real-Time Expense Calibration

Static budgets set fixed allocations that limit responsiveness to fluctuating costs, whereas flexible spending plans enable real-time expense calibration by adjusting budget limits based on actual financial performance and operational changes. This adaptability enhances financial control by allowing precise resource allocation and minimizing variances between projected and actual expenditures.

Automated Budget Variance Alerts

Automated budget variance alerts enhance financial control by instantly identifying deviations between a static budget and actual expenses, enabling timely adjustments within a flexible spending plan. This real-time monitoring ensures organizations maintain spending discipline and optimize resource allocation efficiently.

Static Budget vs Flexible Spending Plan for financial control. Infographic