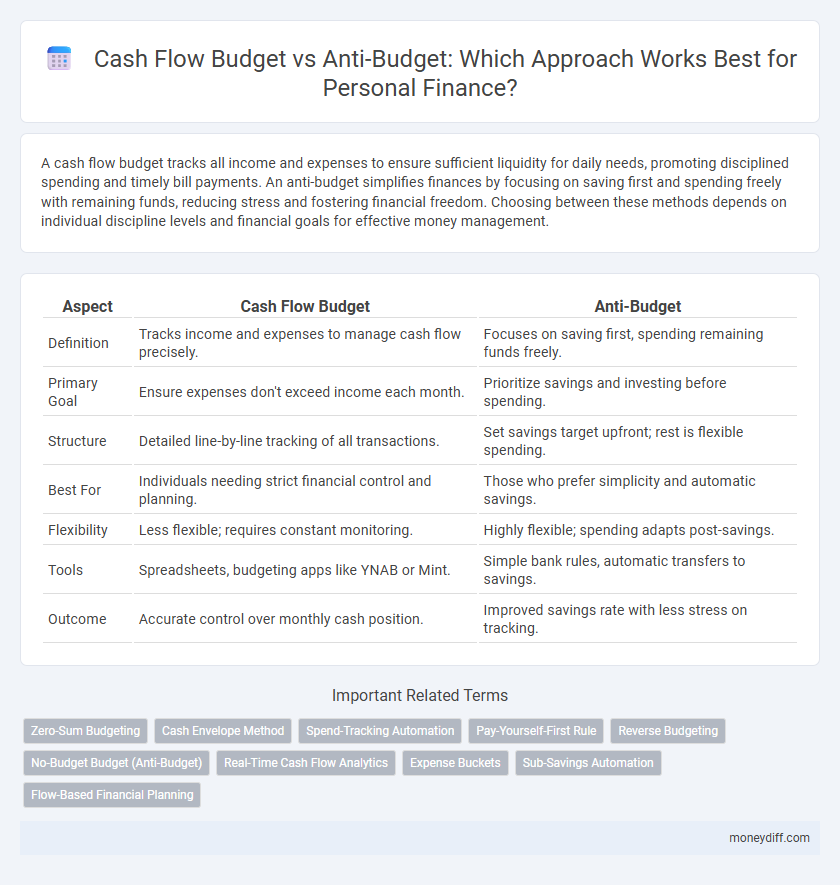

A cash flow budget tracks all income and expenses to ensure sufficient liquidity for daily needs, promoting disciplined spending and timely bill payments. An anti-budget simplifies finances by focusing on saving first and spending freely with remaining funds, reducing stress and fostering financial freedom. Choosing between these methods depends on individual discipline levels and financial goals for effective money management.

Table of Comparison

| Aspect | Cash Flow Budget | Anti-Budget |

|---|---|---|

| Definition | Tracks income and expenses to manage cash flow precisely. | Focuses on saving first, spending remaining funds freely. |

| Primary Goal | Ensure expenses don't exceed income each month. | Prioritize savings and investing before spending. |

| Structure | Detailed line-by-line tracking of all transactions. | Set savings target upfront; rest is flexible spending. |

| Best For | Individuals needing strict financial control and planning. | Those who prefer simplicity and automatic savings. |

| Flexibility | Less flexible; requires constant monitoring. | Highly flexible; spending adapts post-savings. |

| Tools | Spreadsheets, budgeting apps like YNAB or Mint. | Simple bank rules, automatic transfers to savings. |

| Outcome | Accurate control over monthly cash position. | Improved savings rate with less stress on tracking. |

Understanding Cash Flow Budget: Key Concepts

A Cash Flow Budget tracks all income and expenses over a specific period, enabling precise management of personal finances by forecasting surplus or deficits. It highlights timing differences between cash inflows and outflows, helping to avoid shortfalls and plan for savings or investments. Understanding key components like recurring income, fixed expenses, and variable costs ensures effective cash flow control and financial stability.

What is the Anti-Budget Approach?

The Anti-Budget approach simplifies personal finance by focusing on automatic savings and essential expenses rather than tracking every dollar spent. This method sets aside a fixed amount for savings upfront, leaving the remaining funds to be spent freely, reducing stress and decision fatigue. It contrasts with traditional cash flow budgets that require detailed tracking and categorizing of income and expenses to manage finances.

Core Differences Between Cash Flow Budget and Anti-Budget

A cash flow budget tracks every dollar of income and expense to ensure spending does not exceed earnings, emphasizing detailed financial management and forecasting. In contrast, an anti-budget prioritizes saving first by automatically allocating a fixed amount to savings before allowing flexible spending of the remaining funds, promoting simplicity and higher savings rates. These core differences highlight the cash flow budget's structure and control versus the anti-budget's focus on spending freedom and savings discipline.

Pros and Cons of Cash Flow Budgeting

Cash flow budgeting provides a clear overview of income and expenses, aiding in effective money management and preventing overspending by forecasting cash availability. It offers flexibility and real-time adjustment possibilities but requires consistent tracking and time investment, which can be challenging for individuals with irregular income. While it enhances control and financial awareness, reliance on precise data makes it less forgiving to unexpected expenses or income fluctuations.

Advantages and Drawbacks of the Anti-Budget

The Anti-Budget simplifies personal finance by allowing individuals to spend freely until essential expenses and savings goals are met, reducing stress and increasing financial flexibility. Its primary advantage is fostering a more relaxed approach without rigid categories, but its drawback lies in potential overspending or lack of awareness about discretionary expenses. This method suits those who prefer intuitive money management but requires discipline to maintain savings and avoid financial pitfalls.

Who Should Use Cash Flow Budgeting?

Cash flow budgeting is ideal for individuals who need detailed tracking of income and expenses to prevent overspending and ensure timely bill payments. Those with irregular income streams, such as freelancers or commission-based workers, benefit from cash flow budgets to manage cash availability throughout the month. People seeking to improve financial discipline and avoid debt accumulation find cash flow budgeting particularly useful for maintaining a clear overview of money inflows and outflows.

Is the Anti-Budget Right for You?

A cash flow budget tracks every dollar of income and expenses to provide detailed control over your finances, ideal for those who prefer structure and accountability. The anti-budget emphasizes spending only on needs and saving the rest, offering simplicity and flexibility for individuals who find traditional budgeting restrictive. Choosing the anti-budget depends on your discipline and financial goals; it suits people who want a less detailed approach but still aim to increase savings without tracking every expense.

Practical Steps to Start a Cash Flow Budget

Creating a cash flow budget begins with tracking all sources of income and categorizing every expense to understand where money is going each month. Utilize budgeting tools or spreadsheets to record daily transactions, enabling accurate forecasting of future cash flow and identifying spending patterns. Setting realistic spending limits based on this data helps manage finances effectively, contrasting with the anti-budget approach by emphasizing proactive cash management rather than passive spending.

Implementing the Anti-Budget: A Simple Guide

Implementing the Anti-Budget involves tracking only essential expenses like rent, utilities, and groceries while allowing flexible spending on non-essentials, promoting financial awareness without rigid restrictions. This method simplifies cash flow management by focusing on maintaining a positive balance rather than itemizing every purchase. By prioritizing core expenses and monitoring account balances regularly, the Anti-Budget fosters sustainable spending habits and reduces the stress of traditional budgeting.

Choosing Between Cash Flow Budget and Anti-Budget for Better Personal Finance

Choosing between a cash flow budget and an anti-budget depends on your financial discipline and goals; a cash flow budget tracks every income and expense for detailed control, while an anti-budget focuses on saving first and spending freely afterward. Cash flow budgeting suits those who need structured planning and accountability to avoid overspending, whereas anti-budgeting benefits individuals seeking simplicity and automatic savings growth. Evaluating personal spending habits and financial priorities helps determine which method optimizes cash management and supports long-term financial stability.

Related Important Terms

Zero-Sum Budgeting

Zero-Sum Budgeting allocates every dollar of income to specific expenses, savings, or debt payments, ensuring the cash flow budget balances to zero each month. This method contrasts with the Anti-Budget, which tracks spending post-hoc without strict allocation, making Zero-Sum Budgeting a proactive tool for personal finance control and optimized cash flow management.

Cash Envelope Method

The Cash Flow Budget method tracks income and expenses to maintain a positive cash balance, while the Anti-Budget emphasizes spending only what remains after saving. The Cash Envelope Method supports cash flow budgeting by allocating physical cash to categories, promoting disciplined spending and preventing overspending in personal finance management.

Spend-Tracking Automation

Cash flow budgets emphasize precise tracking of income and expenses to forecast available funds, while anti-budgets prioritize automatic spending limits without detailed categorization, streamlining personal finance management. Spend-tracking automation enhances both methods by providing real-time insights and reducing manual input, enabling more accurate financial decisions and improved cash flow control.

Pay-Yourself-First Rule

A Cash Flow Budget centers on tracking income and expenses to maintain control over spending, while the Anti-Budget simplifies finances by focusing only on saving first through the Pay-Yourself-First rule, allocating a fixed amount to savings before any other expenses. This method enhances disciplined wealth building by prioritizing automated savings and reducing decision fatigue in personal finance management.

Reverse Budgeting

Reverse budgeting prioritizes saving and investing by allocating funds to financial goals first, then using the remaining income for expenses, contrasting with traditional cash flow budgets that plan expenses before savings. This method enhances personal finance management by ensuring consistent saving habits and reducing unnecessary spending, leading to better long-term wealth accumulation.

No-Budget Budget (Anti-Budget)

The No-Budget Budget, or Anti-Budget, simplifies personal finance by setting a fixed savings amount first and allowing unrestricted spending of the remaining income, promoting financial freedom without detailed expense tracking. This approach contrasts with traditional Cash Flow Budgets that require meticulous categorization of every expense, making the Anti-Budget ideal for individuals seeking low-maintenance money management and stress-free spending habits.

Real-Time Cash Flow Analytics

Real-time cash flow analytics in a cash flow budget provide continuous tracking of income and expenses, enabling precise financial decision-making and preventing overspending. Anti-budget methods focus on flexible spending limits without strict tracking, but lack the detailed insights of real-time cash flow data that optimize personal financial control.

Expense Buckets

Cash Flow Budget categorizes expenses into fixed, variable, and discretionary buckets, enabling precise tracking of income versus outflow, while Anti-Budget simplifies personal finance by focusing only on savings and spending limits without detailed buckets. Expense buckets in a Cash Flow Budget help identify spending patterns and optimize cash management; in contrast, the Anti-Budget minimizes budgeting friction by setting broad categories like "essentials" and "wants" to encourage financial flexibility.

Sub-Savings Automation

Cash flow budgets track income and expenses to manage money effectively, while anti-budgets emphasize spending only on essentials and saving the rest, promoting financial freedom. Sub-savings automation enhances both methods by automatically allocating funds to specific savings goals, reducing manual effort and improving consistency in building emergency funds, investments, or debt repayment.

Flow-Based Financial Planning

Cash Flow Budget emphasizes tracking income and expenses to ensure liquidity and avoid shortfalls, while Anti-Budget focuses on pre-allocating funds to priorities by automatically directing cash flows toward savings and investments. Flow-Based Financial Planning simplifies management by aligning spending with real-time cash availability, promoting disciplined saving habits without rigid expense categories.

Cash Flow Budget vs Anti-Budget for personal finance. Infographic