The Budget method involves tracking income and expenses to allocate funds for specific categories, ensuring balanced spending and savings. The Pay-Yourself-First method prioritizes saving by setting aside a predetermined amount before covering expenses, fostering disciplined wealth accumulation. Choosing between these approaches depends on individual financial goals and spending habits.

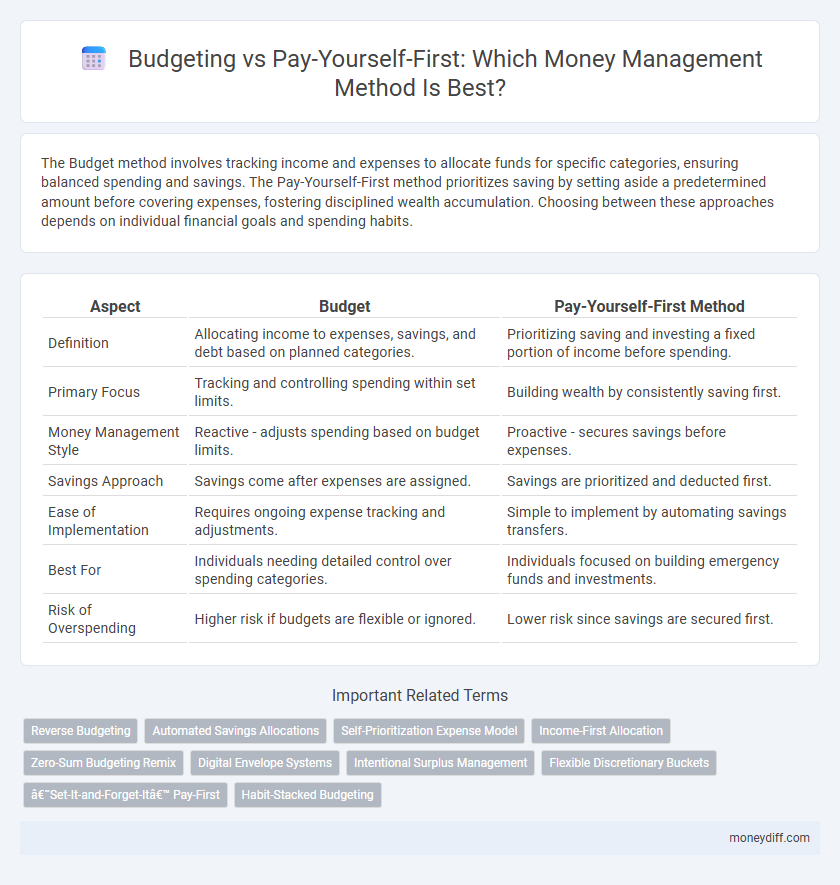

Table of Comparison

| Aspect | Budget | Pay-Yourself-First Method |

|---|---|---|

| Definition | Allocating income to expenses, savings, and debt based on planned categories. | Prioritizing saving and investing a fixed portion of income before spending. |

| Primary Focus | Tracking and controlling spending within set limits. | Building wealth by consistently saving first. |

| Money Management Style | Reactive - adjusts spending based on budget limits. | Proactive - secures savings before expenses. |

| Savings Approach | Savings come after expenses are assigned. | Savings are prioritized and deducted first. |

| Ease of Implementation | Requires ongoing expense tracking and adjustments. | Simple to implement by automating savings transfers. |

| Best For | Individuals needing detailed control over spending categories. | Individuals focused on building emergency funds and investments. |

| Risk of Overspending | Higher risk if budgets are flexible or ignored. | Lower risk since savings are secured first. |

Understanding Traditional Budgeting Methods

Traditional budgeting methods focus on allocating income into specific categories such as housing, food, and entertainment to control spending and achieve financial goals. These methods often require detailed tracking of expenses and adjustments to stay within set limits. Compared to the Pay-Yourself-First approach, traditional budgeting emphasizes reactive spending control rather than proactive saving prioritization.

What is the Pay-Yourself-First Approach?

The Pay-Yourself-First approach prioritizes saving a predetermined portion of income before allocating funds to expenses, ensuring consistent wealth accumulation. Unlike traditional budgeting, which plans spending first and saves what's left, this method secures financial goals by treating savings as a mandatory expense. Automating transfers to savings or investment accounts guarantees disciplined money management and long-term financial stability.

Key Differences: Budgeting vs Pay-Yourself-First

Budgeting involves allocating specific amounts to various spending categories, tracking expenses, and adjusting to stay within limits, providing a comprehensive overview of income and expenditures. The Pay-Yourself-First method prioritizes saving a fixed portion of income before any spending, ensuring consistent savings and financial discipline. While budgeting offers detailed control over all financial aspects, the Pay-Yourself-First approach simplifies money management by focusing primarily on saving goals.

Benefits of Standard Budgeting for Financial Control

Standard budgeting offers precise tracking of income and expenses, enabling individuals to allocate funds effectively and avoid overspending. It provides a structured framework for setting financial goals and monitoring progress, promoting disciplined saving habits. This method enhances financial control by creating clear spending limits, reducing impulsive purchases and increasing overall financial stability.

Advantages of the Pay-Yourself-First Strategy

The Pay-Yourself-First method prioritizes saving by automatically setting aside a portion of income before other expenses, ensuring consistent wealth accumulation and financial security. This strategy reduces the temptation to overspend, promotes disciplined money management, and helps build emergency funds or investment capital faster. Unlike traditional budgeting, it simplifies decision-making by focusing on savings first, making financial goals more achievable and sustainable.

Potential Drawbacks of Both Methods

The budget method can lead to inflexibility, causing stress when unexpected expenses arise or when categories are too rigidly defined. The Pay-Yourself-First method risks underfunding essential bills or debt repayments if savings goals are prioritized excessively. Both approaches require careful adjustment to balance short-term needs and long-term financial health effectively.

Choosing the Right Method for Your Financial Goals

Selecting the right money management method depends on your financial goals and spending habits. The Budget approach offers detailed tracking and control over expenses, ideal for those needing discipline and clear spending limits. Pay-Yourself-First prioritizes savings and investments by automatically allocating funds, best suited for individuals focused on wealth building and long-term financial security.

Combining Budgeting and Pay-Yourself-First for Success

Combining budgeting with the pay-yourself-first method maximizes financial discipline by ensuring savings targets are prioritized before expenses. Allocating a fixed percentage of income to savings upfront, then adjusting the budget around remaining funds, creates a balanced approach that enhances both spending control and wealth accumulation. This hybrid strategy fosters consistent saving habits while maintaining flexibility to manage daily expenses effectively.

Case Studies: Real-Life Applications of Both Methods

Case studies reveal that individuals using the Budget method often gain detailed control over monthly expenses, allowing precise adjustments to meet financial goals. In comparison, real-life applications of the Pay-Yourself-First method demonstrate accelerated savings growth by prioritizing automatic transfers to savings before spending. Data from these case studies indicate that combining both methods can optimize cash flow management and improve long-term wealth accumulation.

Expert Tips for Effective Money Management

Implementing the Pay-Yourself-First method ensures consistent savings by prioritizing automatic transfers to savings accounts before expenses. Experts recommend combining this strategy with a detailed budget to track discretionary spending and avoid overspending. Using apps that sync income and expenses offers real-time insights, enhancing financial discipline and goal achievement.

Related Important Terms

Reverse Budgeting

Reverse budgeting prioritizes saving and investing by setting aside a predetermined amount before allocating funds for expenses, ensuring financial goals are met first. This method contrasts with traditional budgets that track spending first, often leading to inconsistent savings and spending habits.

Automated Savings Allocations

Automated savings allocations in the Pay-Yourself-First method prioritize setting aside a fixed percentage of income before any expenses, ensuring consistent growth of emergency funds and investments. Traditional budgeting often allocates leftover money after expenses, which can lead to irregular savings and missed financial goals.

Self-Prioritization Expense Model

The Self-Prioritization Expense Model emphasizes allocating income towards savings and investments before addressing discretionary spending, ensuring financial goals are met consistently. Unlike traditional budgets that restrict spending categories, this method promotes disciplined money management by prioritizing personal wealth growth and financial security.

Income-First Allocation

Income-First Allocation prioritizes saving or investing a fixed percentage of income immediately upon receipt, aligning with the Pay-Yourself-First method to ensure financial goals are met before discretionary spending. Unlike traditional budgeting that allocates expenses first, this strategy enhances disciplined saving and long-term wealth accumulation by treating savings as a mandatory expense.

Zero-Sum Budgeting Remix

Zero-Sum Budgeting Remix allocates every dollar of income to specific expenses, savings, or debt repayment, ensuring no money is left unassigned and promoting disciplined financial control. This method contrasts with Pay-Yourself-First by prioritizing comprehensive expense planning before saving, enhancing cash flow visibility and preventing overspending.

Digital Envelope Systems

Digital envelope systems enhance the pay-yourself-first method by automatically allocating funds into categorized virtual envelopes for expenses, savings, and investments, ensuring disciplined money management. This approach offers real-time tracking and flexibility compared to traditional budgeting, promoting efficient financial goal achievement.

Intentional Surplus Management

The Pay-Yourself-First method prioritizes automatic savings by setting aside a predetermined amount before any expenses, ensuring intentional surplus management and financial discipline. In contrast, traditional budgeting allocates funds after expenses, often risking undersaving and reactive adjustments rather than proactive surplus creation.

Flexible Discretionary Buckets

Flexible discretionary buckets in the Pay-Yourself-First method allow individuals to allocate surplus income toward variable spending categories, enhancing adaptability in financial planning compared to rigid budget categories. This approach promotes financial discipline by prioritizing savings and investments before discretionary spending, ensuring long-term wealth growth while accommodating lifestyle changes.

‘Set-It-and-Forget-It’ Pay-First

The Pay-Yourself-First method simplifies money management by automatically allocating a predetermined portion of income to savings or investments before covering expenses, ensuring consistent financial growth. Unlike traditional budgeting, this 'Set-It-and-Forget-It' strategy minimizes decision fatigue and promotes disciplined saving habits without constant tracking or adjustments.

Habit-Stacked Budgeting

Habit-stacked budgeting integrates the pay-yourself-first method by automatically allocating savings and essential expenses into distinct categories, promoting consistent financial discipline. This approach leverages behavioral triggers to reinforce positive money management habits, ensuring funds are prioritized for saving before discretionary spending.

Budget vs Pay-Yourself-First Method for money management. Infographic