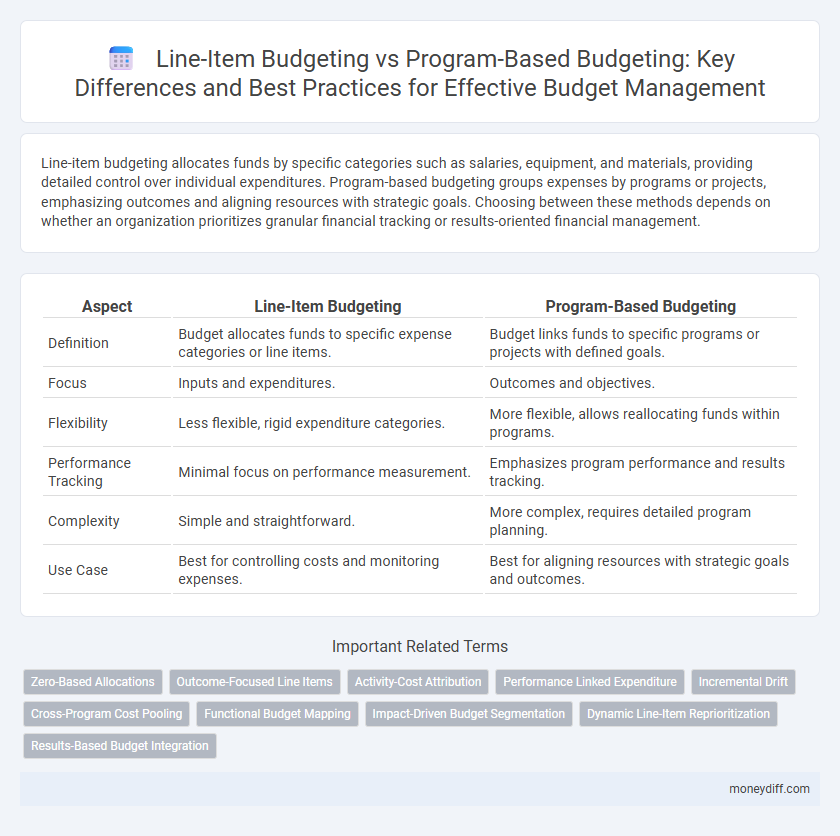

Line-item budgeting allocates funds by specific categories such as salaries, equipment, and materials, providing detailed control over individual expenditures. Program-based budgeting groups expenses by programs or projects, emphasizing outcomes and aligning resources with strategic goals. Choosing between these methods depends on whether an organization prioritizes granular financial tracking or results-oriented financial management.

Table of Comparison

| Aspect | Line-Item Budgeting | Program-Based Budgeting |

|---|---|---|

| Definition | Budget allocates funds to specific expense categories or line items. | Budget links funds to specific programs or projects with defined goals. |

| Focus | Inputs and expenditures. | Outcomes and objectives. |

| Flexibility | Less flexible, rigid expenditure categories. | More flexible, allows reallocating funds within programs. |

| Performance Tracking | Minimal focus on performance measurement. | Emphasizes program performance and results tracking. |

| Complexity | Simple and straightforward. | More complex, requires detailed program planning. |

| Use Case | Best for controlling costs and monitoring expenses. | Best for aligning resources with strategic goals and outcomes. |

Understanding Line-Item Budgeting

Line-item budgeting allocates funds by categorizing expenses into specific accounts or "lines," such as salaries, supplies, and equipment, providing detailed financial tracking. This method simplifies monitoring expenditures and ensures accountability by outlining exact spending limits for each category. While it emphasizes control and transparency, line-item budgeting may lack flexibility for adapting to programmatic changes or performance outcomes.

What Is Program-Based Budgeting?

Program-Based Budgeting allocates resources according to specific programs or objectives, linking funds directly to outcomes and strategic goals. Unlike traditional Line-Item Budgeting, which categorizes expenses by inputs such as salaries or supplies, Program-Based Budgeting emphasizes performance and accountability by focusing on results. This approach enhances transparency and resource optimization for government agencies and organizations aiming to achieve measurable impacts.

Key Differences Between Line-Item and Program-Based Budgeting

Line-item budgeting categorizes expenses by individual items such as salaries, office supplies, and equipment, allowing for straightforward tracking of specific cost elements. Program-based budgeting organizes funds according to programs or projects, emphasizing objectives and outcomes rather than detailed expenditures. Key differences include the scope of focus--line-item budgeting centers on input control while program-based budgeting prioritizes performance and results measurement.

Advantages of Line-Item Budgeting

Line-item budgeting offers precise control and accountability by categorizing expenses into specific accounts, facilitating straightforward tracking and preventing overspending. It simplifies financial reporting and auditing processes through detailed expense categorization, enabling easier identification of budget variances. Government agencies and organizations benefit from this approach due to its transparency and ease of implementation in managing public funds.

Benefits of Program-Based Budgeting

Program-based budgeting enhances resource allocation by linking expenditures directly to specific government programs and outcomes, improving transparency and accountability. It facilitates strategic planning by aligning financial resources with prioritized objectives, enabling more effective performance measurement and evaluation. This approach supports better decision-making and promotes efficient use of funds by highlighting program effectiveness and impact.

Challenges of Line-Item Budgeting

Line-item budgeting faces challenges such as limited flexibility and difficulty in linking expenditures to specific program outcomes, which can hinder strategic resource allocation. This traditional approach often results in a focus on controlling costs rather than evaluating efficiency or effectiveness. Moreover, it provides minimal insight into the impact of spending, making it harder for organizations to align budgets with broader goals.

Limitations of Program-Based Budgeting

Program-based budgeting often struggles with accurately capturing detailed expenditure data, leading to less transparency compared to line-item budgeting. Its complexity can result in implementation challenges, especially in organizations lacking robust data systems and trained personnel. This approach may also obscure specific cost control and accountability due to aggregated program costs rather than granular line-item tracking.

When to Use Line-Item vs Program-Based Budgeting

Line-item budgeting is ideal for organizations requiring detailed tracking of expenses by specific categories, such as salaries, supplies, and equipment, ensuring strict financial control and accountability. Program-based budgeting suits entities focused on strategic outcomes and performance measurement, allocating funds based on distinct programs or projects aligned with organizational goals. Choosing line-item budgeting is best when detailed oversight of individual cost components is necessary, while program-based budgeting excels in contexts prioritizing outcome-driven resource allocation and evaluation.

Impact on Financial Accountability

Line-item budgeting enhances financial accountability by providing detailed tracking of expenditures against specific categories, allowing organizations to monitor spending closely and prevent overspending. Program-based budgeting improves accountability by linking financial resources to outcomes and objectives, facilitating performance evaluation and ensuring funds are used effectively to achieve strategic goals. Organizations often combine both approaches to balance detailed fiscal control with results-oriented financial management.

Choosing the Right Budgeting Approach for Your Needs

Line-item budgeting provides detailed control by allocating funds to specific categories, making it ideal for organizations prioritizing accountability and straightforward tracking. Program-based budgeting focuses on outcomes by linking expenditures to specific programs and objectives, benefiting entities aiming to assess performance and impact. Select line-item budgeting for precise expense management or program-based budgeting to align financial resources with strategic goals and measurable results.

Related Important Terms

Zero-Based Allocations

Line-item budgeting provides detailed tracking of expenses by category, which helps identify areas for zero-based allocations to eliminate unnecessary costs. Program-based budgeting aligns funding with strategic goals, enabling zero-based reviews that reallocate resources based on program performance and outcomes rather than historical spending.

Outcome-Focused Line Items

Outcome-focused line-item budgeting allocates funds based on specific activities and measurable outputs, enhancing accountability and clear financial tracking. Program-based budgeting prioritizes goals and results by funding integrated projects, aligning resources with strategic outcomes for improved effectiveness.

Activity-Cost Attribution

Line-item budgeting allocates funds based on individual expense categories, emphasizing detailed tracking of specific costs such as salaries, supplies, and equipment; program-based budgeting assigns costs to activities or programs, enhancing clarity in linking expenditures to intended outcomes and facilitating performance evaluation. Activity-cost attribution in program-based budgeting improves resource allocation efficiency by directly associating expenses with program objectives, unlike line-item budgeting which often obscures cost-effectiveness due to its granular yet segmented nature.

Performance Linked Expenditure

Line-item budgeting allocates funds based on specific expense categories, offering clear accountability but limited insight into performance outcomes, while program-based budgeting links expenditure directly to program goals and results, enhancing efficiency and enabling performance-driven resource allocation. Performance-linked expenditure under program-based budgeting facilitates better monitoring and evaluation of budget impact on service delivery and strategic objectives.

Incremental Drift

Line-item budgeting often leads to incremental drift by perpetuating past allocations without critically assessing the effectiveness of expenditures, resulting in gradual budget inefficiencies. Program-based budgeting mitigates incremental drift by aligning resources with measurable program outcomes, enabling more strategic adjustments and enhancing fiscal accountability.

Cross-Program Cost Pooling

Line-item budgeting allocates funds by specific categories such as salaries and supplies, limiting flexibility in addressing costs shared across multiple programs, whereas program-based budgeting enables cross-program cost pooling to optimize resource allocation and improve overall financial management. Cross-program cost pooling consolidates indirect expenses like administrative support and facility maintenance, enhancing transparency and efficiency in budget planning and execution.

Functional Budget Mapping

Line-item budgeting allocates funds to specific expense categories, providing clear, detailed tracking of costs but limiting flexibility in resource reallocation. Program-based budgeting emphasizes functional budget mapping by grouping expenditures according to program goals, enhancing alignment with organizational objectives and improving outcome-based financial management.

Impact-Driven Budget Segmentation

Line-item budgeting allocates funds to specific categories such as salaries, equipment, and supplies, enabling precise tracking of expenditures but often lacking insight into overall program outcomes. Program-based budgeting organizes financial resources around specific programs or objectives, fostering impact-driven budget segmentation by linking spending directly to performance metrics and strategic goals.

Dynamic Line-Item Reprioritization

Dynamic line-item reprioritization in line-item budgeting allows organizations to adjust financial allocations quickly within predefined categories, enhancing responsiveness to changing needs. Unlike program-based budgeting, which allocates funds based on specific objectives or outcomes, dynamic line-item reprioritization provides granular control over expenditures, optimizing resource utilization without overhauling the entire budget structure.

Results-Based Budget Integration

Line-item budgeting allocates funds based on specific expense categories, offering clear financial control but limited insight into performance outcomes, whereas program-based budgeting aligns resources with strategic objectives and focuses on achieving measurable results. Integrating results-based budgeting enhances program-based approaches by linking financial inputs to performance indicators, enabling more effective monitoring and evaluation of budget impact.

Line-Item Budgeting vs Program-Based Budgeting for Budget Infographic