Budgeting involves allocating your total income into specific categories, while sub-savings budgeting breaks these categories down further into smaller, targeted savings goals. This method enhances financial control by tracking progress on distinct objectives, such as emergency funds or vacation savings, within the broader budget framework. Implementing sub-savings budgeting promotes disciplined spending and helps achieve both short-term and long-term financial targets more effectively.

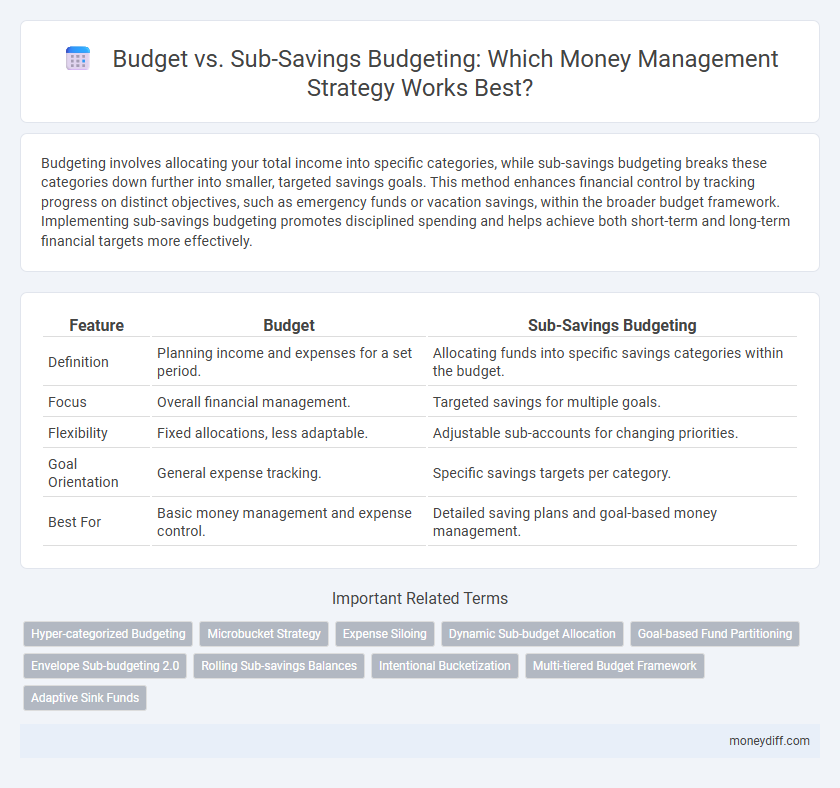

Table of Comparison

| Feature | Budget | Sub-Savings Budgeting |

|---|---|---|

| Definition | Planning income and expenses for a set period. | Allocating funds into specific savings categories within the budget. |

| Focus | Overall financial management. | Targeted savings for multiple goals. |

| Flexibility | Fixed allocations, less adaptable. | Adjustable sub-accounts for changing priorities. |

| Goal Orientation | General expense tracking. | Specific savings targets per category. |

| Best For | Basic money management and expense control. | Detailed saving plans and goal-based money management. |

Understanding Traditional Budgeting

Traditional budgeting involves allocating fixed amounts of income to specific expense categories, emphasizing strict spending limits to control finances. This method helps track cash flow and ensures that essential expenses are covered, reducing the risk of overspending. However, traditional budgeting may lack flexibility for unexpected costs compared to sub-savings budgeting, which divides funds into multiple saving goals within the budget.

What is Sub-Savings Budgeting?

Sub-Savings Budgeting is a money management technique that divides a main budget into multiple smaller, goal-specific savings accounts or categories. This method allows for precise tracking and allocation of funds towards distinct financial objectives such as emergency funds, vacation expenses, or debt repayment. By segmenting savings, Sub-Savings Budgeting enhances financial discipline and ensures funds are reserved for prioritized goals.

Key Differences Between Budgeting Methods

Budgeting focuses on allocating income to expenses and savings, emphasizing control over spending within set limits, while sub-savings budgeting breaks down savings into specific categories for targeted financial goals. The key difference lies in how funds are categorized: traditional budgeting pools savings together, whereas sub-savings budgeting designates separate funds for goals like emergency funds, vacations, or debt repayment. This granular approach in sub-savings budgeting enhances goal specificity and progress tracking compared to the broader allocation in standard budgeting.

Pros and Cons of Traditional Budgeting

Traditional budgeting provides clear structure and control over expenses, helping users plan monthly income allocation effectively. It can be rigid and time-consuming, often leading to frustration when unexpected expenses occur or goals shift. While it promotes discipline, its lack of flexibility may hinder adapting to dynamic financial situations compared to sub-savings budgeting.

Advantages of Sub-Savings Budgeting

Sub-savings budgeting enables precise tracking of expenses by allocating funds into specific sub-categories, fostering better financial discipline and preventing overspending. This method enhances goal-oriented savings, allowing individuals to accumulate money for multiple purposes simultaneously, such as emergencies, vacations, and debt repayment. By promoting transparency and control over each spending area, sub-savings budgeting significantly improves overall money management efficiency compared to traditional general budgeting.

Customizing Budgets for Personal Goals

Customizing budgets for personal goals enhances money management by aligning spending with individual priorities, using category-specific allocations within a primary budget or employing sub-savings budgets for targeted savings. Sub-savings budgeting enables users to create separate savings pools for distinct objectives, such as emergency funds, vacations, or debt repayment, improving financial discipline and goal tracking. Integrating these approaches allows for dynamic flexibility, ensuring budgets adapt to evolving financial goals and optimize resource allocation for maximum effectiveness.

Common Mistakes in Budget and Sub-Savings Approaches

Confusing a traditional budget with sub-savings budgeting often leads to overlapping expense categories and inadequate tracking of discretionary funds. A common mistake is neglecting to allocate clear sub-savings for specific goals, causing funds to bleed into general expenses and undermining long-term financial objectives. Failure to adjust sub-savings contributions during fluctuating income periods results in inconsistent savings growth and budget instability.

Which Method Suits Different Money Management Styles?

Budgeting suits individuals who prefer structured financial plans with clear limits on spending categories, ensuring disciplined money management and goal tracking. Sub-savings budgeting appeals to those who favor flexibility, allowing money to be allocated into various saving pots for specific goals without strict category constraints. Choosing between these methods depends on whether one values detailed expense control or adaptable saving strategies for effective financial management.

Practical Steps to Implement Each Approach

Establishing a comprehensive budget involves categorizing income and assigning specific spending limits to each expense group, enabling clear tracking and control of expenditures. In contrast, sub-savings budgeting focuses on dividing savings into targeted sub-accounts for goals such as emergencies, vacations, or education, facilitating disciplined fund allocation. To implement these approaches effectively, use budgeting apps to monitor spending against budgets and automate transfers to designated sub-savings accounts for consistent goal-oriented saving.

Making Your Money Work: Final Recommendations

Optimizing money management requires distinguishing between a comprehensive budget and sub-savings budgeting to maximize financial control. A detailed budget tracks overall income and expenses, while sub-savings budgeting allocates funds to specific savings goals, enhancing discipline and goal achievement. Prioritizing both strategies ensures efficient resource allocation and strengthens long-term financial stability.

Related Important Terms

Hyper-categorized Budgeting

Hyper-categorized budgeting segments finances into detailed subcategories, enhancing precision and control beyond traditional budgeting by tracking expenses within micro-level sub-savings accounts. This approach improves money management through targeted allocation and real-time monitoring, enabling users to optimize spending and maximize savings effectively.

Microbucket Strategy

The Microbucket Strategy divides a main budget into smaller, targeted sub-savings buckets, allowing for precise tracking and allocation of funds toward specific goals such as emergency funds, vacation, and debt repayment. This method enhances financial discipline by promoting clarity and control over spending compared to traditional budget structures.

Expense Siloing

Budgeting segments expenses into distinct categories to monitor spending and maintain financial control, while sub-savings budgeting further isolates funds within these categories to allocate money for specific goals or unexpected costs. Expense siloing enhances money management by preventing overspending in one area from affecting others, promoting disciplined saving and targeted financial planning.

Dynamic Sub-budget Allocation

Dynamic sub-budget allocation enhances money management by enabling real-time adjustments within a primary budget, optimizing fund distribution across categories based on shifting priorities and expenses. This approach increases financial flexibility and control, ensuring efficient use of resources while preventing overspending in specific sub-savings areas.

Goal-based Fund Partitioning

Goal-based fund partitioning in budgeting enhances financial clarity by allocating specific amounts to primary categories like essentials, savings, and discretionary spending, whereas sub-savings budgeting further divides savings into targeted goals such as emergency funds, retirement, and vacations. This structured approach optimizes money management by ensuring disciplined fund distribution aligned with personalized financial objectives.

Envelope Sub-budgeting 2.0

Envelope Sub-budgeting 2.0 enhances money management by dividing funds into specific sub-savings categories within the main budget, allowing for precise tracking and controlled spending across multiple financial goals. This method improves cash flow visibility, reduces overspending, and promotes disciplined saving by assigning exact amounts to each sub-envelope, unlike traditional budgeting which often aggregates expenses.

Rolling Sub-savings Balances

Rolling sub-savings balances enhance money management by continuously reallocating unused funds within a budget, ensuring optimal liquidity and preventing overspending. This dynamic approach improves financial flexibility compared to static budget categories by allowing seamless adjustment of sub-savings targets based on real-time financial needs.

Intentional Bucketization

Intentional bucketization divides a budget into specific sub-savings categories, enabling targeted allocation for distinct financial goals such as emergency funds, vacations, or debt repayment. This method enhances money management by promoting disciplined savings and preventing overspending across separate needs, contrasting with broad budget models that treat all funds as a single pool.

Multi-tiered Budget Framework

A multi-tiered budget framework distinguishes between primary budget allocation and sub-savings budgeting, allowing for more precise tracking and management of funds by segmenting spending categories into hierarchical layers. This approach enhances financial control by enabling targeted savings goals within sub-categories, improving overall money management efficiency.

Adaptive Sink Funds

Adaptive Sink Funds optimize money management by allocating specific savings for future, anticipated expenses, distinct from the overall budget, ensuring financial flexibility without disrupting monthly cash flow. This targeted approach enhances budget accuracy by separating long-term savings goals from everyday spending, reducing the risk of overspending while maintaining liquidity.

Budget vs Sub-Savings Budgeting for money management. Infographic