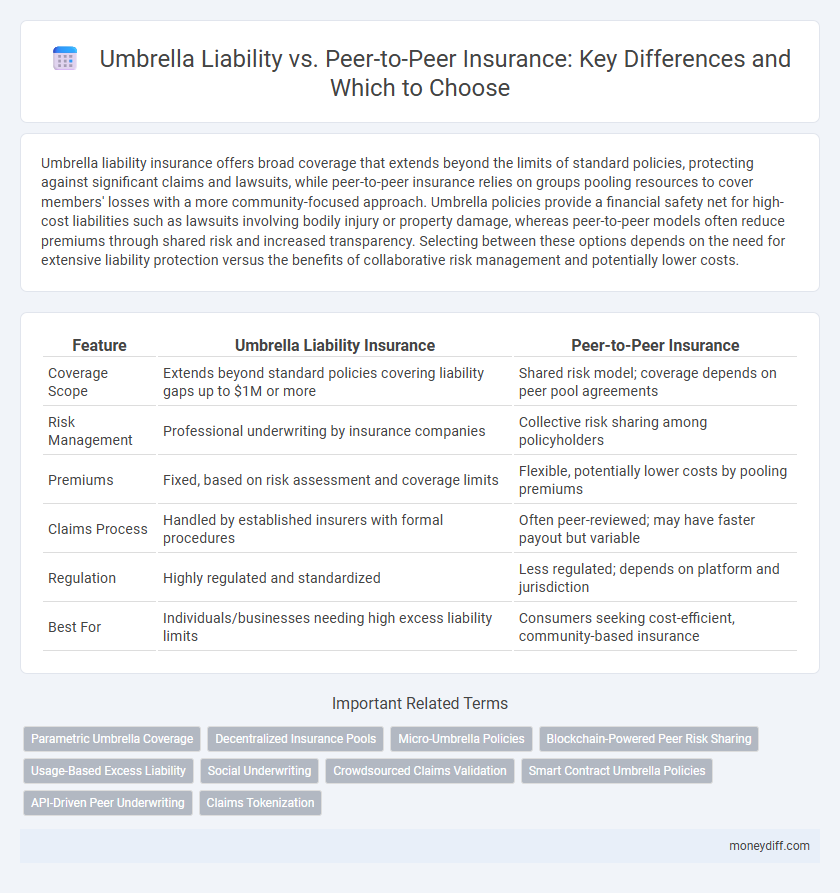

Umbrella liability insurance offers broad coverage that extends beyond the limits of standard policies, protecting against significant claims and lawsuits, while peer-to-peer insurance relies on groups pooling resources to cover members' losses with a more community-focused approach. Umbrella policies provide a financial safety net for high-cost liabilities such as lawsuits involving bodily injury or property damage, whereas peer-to-peer models often reduce premiums through shared risk and increased transparency. Selecting between these options depends on the need for extensive liability protection versus the benefits of collaborative risk management and potentially lower costs.

Table of Comparison

| Feature | Umbrella Liability Insurance | Peer-to-Peer Insurance |

|---|---|---|

| Coverage Scope | Extends beyond standard policies covering liability gaps up to $1M or more | Shared risk model; coverage depends on peer pool agreements |

| Risk Management | Professional underwriting by insurance companies | Collective risk sharing among policyholders |

| Premiums | Fixed, based on risk assessment and coverage limits | Flexible, potentially lower costs by pooling premiums |

| Claims Process | Handled by established insurers with formal procedures | Often peer-reviewed; may have faster payout but variable |

| Regulation | Highly regulated and standardized | Less regulated; depends on platform and jurisdiction |

| Best For | Individuals/businesses needing high excess liability limits | Consumers seeking cost-efficient, community-based insurance |

Understanding Umbrella Liability Insurance

Umbrella liability insurance provides an extra layer of protection by covering claims that exceed the limits of underlying policies like auto or homeowners insurance. It protects assets and future earnings from major lawsuits or catastrophic events, offering broader coverage including personal injury, property damage, and certain liabilities not covered by primary policies. Unlike peer-to-peer insurance, which relies on collective risk sharing within a community, umbrella liability insurance is a traditional, insurer-backed policy designed to safeguard insured individuals from significant financial losses.

What Is Peer-to-Peer Insurance?

Peer-to-peer (P2P) insurance is a decentralized model where groups of individuals pool their premiums to cover collective risks, reducing reliance on traditional insurance companies. This approach fosters transparency, lowers costs, and aligns interests by enabling members to share unclaimed premiums, promoting trust within the community. Unlike umbrella liability insurance, which provides broader coverage beyond standard policies, P2P insurance emphasizes collaborative risk management among peers.

Key Differences Between Umbrella and Peer-to-Peer Insurance

Umbrella liability insurance provides an extra layer of coverage beyond standard policy limits, protecting against large claims or lawsuits, while peer-to-peer insurance pools resources among participants to share risks collaboratively. Umbrella policies are typically offered by traditional insurers with fixed premiums and regulatory oversight, whereas peer-to-peer models rely on group funding, potentially lowering costs and reducing conflicts of interest. Understanding these distinctions helps consumers choose between broad excess liability protection and a community-based risk-sharing approach.

Coverage Scope: Umbrella Liability Explained

Umbrella liability insurance provides an extra layer of coverage beyond the limits of standard auto, home, or renters policies, protecting policyholders against large claims or lawsuits that exceed primary coverage. It typically covers a wide range of risks including bodily injury, property damage, personal injury, and legal defense costs, offering broad protection for significant liability exposures. In contrast, peer-to-peer insurance operates on a shared-risk model with limited coverage scopes, often focusing on specific types of claims within a community without the extensive protection umbrella liability policies deliver.

Community-Based Risk Sharing in Peer-to-Peer Insurance

Peer-to-peer insurance leverages community-based risk sharing by pooling funds among members to cover claims, promoting transparency and lower costs compared to traditional umbrella liability policies. This model reduces reliance on large insurance corporations, allowing participants to benefit from collective risk management and potential premium rebates. Community pooling mechanisms inherent in P2P insurance foster trust and engagement, contrasting with the broader coverage scope but higher premiums typical of umbrella liability insurance.

Cost Comparison: Premiums and Payouts

Umbrella liability insurance typically involves higher premiums due to broader coverage limits and more extensive protection against multiple liability claims, while peer-to-peer insurance often offers lower premiums by distributing risk among a network of participants. Payouts in umbrella liability policies are generally more predictable and substantial, backed by established insurers, whereas peer-to-peer models may provide quicker, community-driven claims resolution but with potentially variable payout amounts. Cost-effectiveness depends on the insured's risk profile, with umbrella policies favoring those seeking comprehensive coverage and peer-to-peer plans appealing to cost-conscious individuals willing to engage in cooperative risk sharing.

Claims Process: Traditional vs Peer-to-Peer

The claims process in traditional umbrella liability insurance typically involves a centralized insurer managing the entire claim, leading to established protocols and faster settlements due to professional handling. Peer-to-peer insurance, however, relies on collective risk-sharing among members, which can result in greater transparency but may experience longer claim resolution times due to decentralized decision-making. Data shows that umbrella liability claims through traditional insurers have an average settlement time of 30 days, whereas peer-to-peer platforms may take up to 45 days depending on member participation.

Flexibility and Customization of Each Insurance Type

Umbrella liability insurance offers broad coverage that extends beyond the limits of standard policies, allowing policyholders to customize their protection against major claims and lawsuits. Peer-to-peer insurance provides flexibility through community-based risk sharing and often lets participants tailor coverage options aligned with their specific needs and risk profiles. Both insurance types offer customizable features, but umbrella liability emphasizes extended protection limits while peer-to-peer focuses on personalized, collaborative risk management.

Which Insurance Fits Your Financial Goals?

Umbrella liability insurance provides extensive coverage beyond standard policies, protecting your assets from large claims and lawsuits, making it ideal for individuals seeking comprehensive financial protection. Peer-to-peer insurance offers a flexible, community-based approach that can lower costs and increase transparency but may have limited coverage compared to traditional umbrella policies. Choosing the right insurance depends on your financial goals, risk tolerance, and desire for coverage limits, with umbrella liability best suited for high net-worth individuals seeking broad protection.

Making the Right Money Management Choice

Umbrella liability insurance offers broad coverage that protects assets beyond the limits of standard policies, making it ideal for those seeking comprehensive risk management. Peer-to-peer insurance leverages collective risk sharing, often resulting in lower premiums but potentially less extensive coverage. Choosing between these options depends on balancing financial protection needs with cost-efficiency and individual risk tolerance.

Related Important Terms

Parametric Umbrella Coverage

Parametric umbrella coverage offers predefined payouts based on verified triggers, providing clear, swift financial protection beyond standard liability limits, unlike traditional peer-to-peer insurance which relies on member contributions and claim approvals. This parametric model enhances risk management efficiency by minimizing claim disputes and accelerating compensation for insured events such as natural disasters or large-scale liabilities.

Decentralized Insurance Pools

Decentralized insurance pools leverage blockchain technology to create peer-to-peer risk-sharing networks, reducing reliance on traditional umbrella liability policies by distributing coverage directly among participants. These pools offer increased transparency, lower premiums, and faster claims processing through smart contracts, challenging conventional insurance models.

Micro-Umbrella Policies

Micro-Umbrella policies offer a cost-effective extension of traditional Umbrella Liability insurance, providing additional liability coverage beyond peer-to-peer insurance limits. These policies bridge coverage gaps, enhancing protection against high-cost claims in peer-to-peer arrangements by supplementing standard liability with broader risk mitigation.

Blockchain-Powered Peer Risk Sharing

Blockchain-powered peer risk sharing transforms traditional umbrella liability insurance by enabling decentralized, transparent pooling of funds where policyholders collectively underwrite risks without intermediaries. This innovative model enhances trust, reduces administrative costs, and offers customizable coverage options tailored to individual risk profiles through smart contracts.

Usage-Based Excess Liability

Usage-based excess liability in umbrella insurance offers broader coverage limits beyond standard policies, providing protection against high-cost claims and lawsuits, while peer-to-peer insurance leverages communal risk-sharing models with usage-based premiums often resulting in cost savings and more personalized coverage. Umbrella liability focuses on extending financial protection for serious incidents, whereas peer-to-peer emphasizes collaborative risk management and transparency through technology-driven usage data.

Social Underwriting

Umbrella liability insurance offers excess coverage over standard policies, protecting against large, unpredictable claims, while peer-to-peer insurance leverages social underwriting to assess risk based on community behavior and trust. Social underwriting in peer-to-peer models enhances transparency and personalized risk evaluation by utilizing social data and group dynamics, potentially reducing fraud and improving claim outcomes.

Crowdsourced Claims Validation

Umbrella liability insurance offers extended protection beyond standard policy limits, providing comprehensive coverage against large or multiple claims, while peer-to-peer insurance leverages crowdsourced claims validation to enhance transparency and reduce fraud. Crowdsourced claims validation in peer-to-peer models utilizes community feedback and real-time data sharing to expedite claim assessments and improve accuracy, contrasting with traditional umbrella policies that rely primarily on insurer-driven evaluations.

Smart Contract Umbrella Policies

Smart contract umbrella policies leverage blockchain technology to automate claims and coverage verification, offering enhanced transparency and efficiency compared to traditional peer-to-peer insurance models. These policies provide layered liability protection beyond underlying limits, reducing disputes through immutable contract execution and real-time risk assessment.

API-Driven Peer Underwriting

API-driven peer underwriting leverages real-time data integration and automated risk assessment to offer more personalized and accurate coverage compared to traditional umbrella liability policies, which provide broad protection over multiple liabilities under a single umbrella. This technology enhances transparency and efficiency by enabling dynamic pricing models and faster claims processing, fundamentally transforming peer-to-peer insurance frameworks.

Claims Tokenization

Claims tokenization in umbrella liability insurance enhances security and transparency by converting claim data into encrypted digital tokens, reducing fraud and streamlining settlement processes. Peer-to-peer insurance leverages blockchain-based tokenization to automate claims verification and payout, fostering trust and efficiency among insured members without traditional intermediaries.

Umbrella Liability vs Peer-to-Peer for insurance. Infographic